3 PREDICTIONS ABOUT THE NIGERIAN FILM INDUSTRY IN 2020

Cinemas houses are springing up regularly and in a a wider variety of locations around Nigeria providing access to more screens for wider…

Cinemas houses are springing up regularly and in a a greater variety of locations around Nigeria — providing more screens to wider parts of the population. Nigerians are also spending more money watching movies whilst homegrown productions are dominating box office revenues. Lastly, increasing distribution opportunities are becoming available to monetize local film content after the theatrical-release cycle.

This is the context in which Nigerian movie industry is entering the new decade. Exciting times. Hence this post making three predictions on what to expect with Nollywood in 2020.

This post is the second in a three part series that will be making 3 predictions about the Nigerian music, movie, and technology industries respectively. The first part, “3 Predictions About the Nigeria Recorded Music Industry in 2020” can be read here.

So, here are my 3 Predictions about the Nigerian Film Industry in 2020.

N1b Movie Budgets

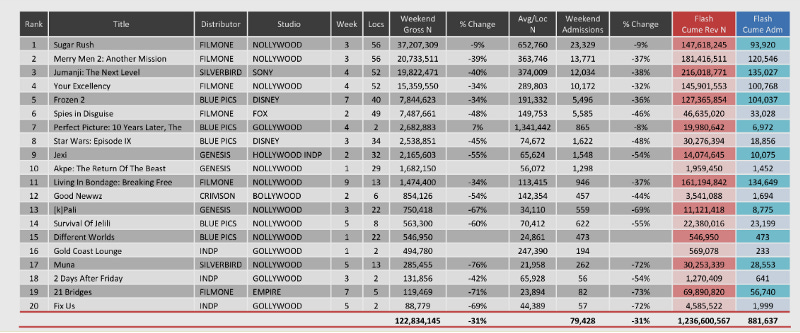

The first reason for this prediction is the increasing returns and expanding revenue sources for big-ticket Nollywood productions. The highest grossing Nollywood movie til date (“The Wedding Party 2”) reportedly cost around N600m/~$1.6m to produce (including marketing). It was financed by the Elfike Film Collective (a joint venture between four leading players in the space). The movie is reported to have generated around N550m/~$1.5m in box office revenues alone.

Assuming the subsequent licence fee paid by Netflix for worldwide digital rights to the film would not have been less than $500k/~N180m licence fee, that would realistically put the movie’s total gross revenues at a minimum of almost N750m/$2m+. Even after any theatrical distribution fees — if any (considering Film One Distribution’s stake in the venture) — that’s potentially a healthy 30%+ return for the four producers to share. In an economic environment with little-to-know access to government securities, deposit savings rates at around 8%-10%, a bear (and volatile) stock market, as well as inflation at 11%+, 30% ROIs are mouth watering. Similar (and even bigger) size returns are also becoming common amongst the medium and lower-mid tier budget productions.

A growing number of movies produced on budgets of between N30m and N70m (marketing costs included) are seeing 2–3x returns on investment — almost entirely driven by box office takings. And Nollywood’s increasing relationship with both local and global VOD platforms is creating more monetization opportunities after the theatrical release run. Local VOD players pay up to $30k/~N10m per movie as licence fees for premium (mid-budget) Nollywood content; global VOD platforms pay 2–3 times as much. As such, expect mid-budget producers to leverage on their past successful projects to access larger funding amounts for bigger productions.

The second reason for this prediction is that, due to the above-discussed ROIs, structured financing opportunities are rapidly developing around Nollywood, thereby increasing the number and variety of sources of for producers to access the necessary funding for their movies. From term loans to more risk-bearing finance (such as joint ventures and film investment funds) the greater the variety of sources, the bigger the potential budgets — at least for the leading production houses.

Budgets for big-ticket Nollywood productions have been getting larger over the last five years, and the number of feature length theatrical releases have been growing. Buoyed by equally growing returns and revenue stream opportunities, Nigerian movie production houses are having the confidence to seek larger sums of investment to finance bigger and bolder movies. Risk mitigation services/distribution arrangements — such as completion bonds and minimum guarantee-based distribution agreements, both of which I have previously written about here — are increasingly being relied upon to protect financiers and assuage their fears.

Additionally, public sector driven funding initiatives (such as the CBN’s CIFI and the Bank of Industry’s “Nollywood Fund”) will only encourage more private sector participation, especially as beneficiaries of these initiatives continue to show positive results in terms of revenues/returns from their financed productions. Add the increasing pressure on banks to lend (due to the 65% LDR policy of the CBN) — and the fact that high-end movie projects are extremely bankable. Expect more funding to pour into big-ticket Nollywood films due to this greater access to funding and, more importantly, due to the next reason for this prediction.

The third reason for this prediction is that the technical quality of Nollywood productions is increasing. Although, in my opinion, scriptwriting and acting are still lagging behind, the overall ‘watchability’ of Nollywood films will continue to grow — especially with more productions aimed at theatrical release which necessitates more engaging and better technically-produced films than those for TV or DVD.

2. International VOD-Financed Nollywood

The first reason for this prediction is the well reported increasing focus on Africa as the next source of growth for global VOD platforms. Netflix’s growing acquisitions of Nollywood content are a testament to this. Netflix — as an example of all the global VOD platforms such as Amazon, Hulu, Canal+ etc — utilises three different methods of acquiring content; and each method reflects a different level of cost/risk/confidence in the content acquired.

Content — that has already been released — can be licensed on a non-exclusive basis. This is the lowest level of content acquisition. It is also the primary means by which most Nollywood content has been brought onto Netflix’s platform ever since “October 1st” and “Fifty” back in 2015 — and attracts the lowest license fees ($40 — $70k on average). Next is where content is licensed on a worldwide (usually excluding Africa) exclusive basis — meaning it has not been prior-released via any medium or in any territory. This type of acquisition attracts higher licence fees ($150 — $200k) due to the exclusivity of the licence involved, which prevents the owner from further monetizing their content online. Genevieve Nnaji’s “Lionheart” was acquired under such a deal.

The final level of acquisition — which I believe will be the basis for some Netflix-distributed Nollywood content in 2020 — is where Netflix itself produces or co-produces exclusively commissioned content branded as a “Netflix Original”. In such scenarios, Netflix would own (or at least co-own) the content and share revenue with (or more likely pay an advance to) the commissioned production house. In contrast to a licence arrangement, in this scenario Netflix and a leading Nollywood production company (eg Ebony Life Pictures, Dioni Visions, Golden Effect Pictures, T.E.N. Africa etc) or consortium would be partner — with a strong production budget provided by Netflix — to produce a movie. Expect such an arrangement to possibly occur in 2020.

The second reason for this prediction is that the global VODs all require more and more premium content to differentiate and compete amongst themselves. However, premium content acquisition costs in developed markets are rising sharply. Tens of billions of dollars are required to even try and keep up with demand — and note that developing stories that can keep a huge user-base continuously engaged is an extremely difficult task. Nollywood, and African content generally, can go a long way towards plugging this anticipated content gap for the VODs.

With thousands of rich and untold stories, and with Nollywood still not quite independently developed enough to tell these stories in a way that can appeal to global audiences, it would seem likely that international producers such as the VODs can partner with our movie creators to deliver these stories as well as possible in the interim. This would be a win win for both the global VODs and the Nollywood community.

The global VODs can acquire/create more premium quality African content at a fraction of the cost of Western and Asian content. As earlier mentioned, premium Nollywood content acquisition costs average around $250k. When compared to the $10–20m fees (each hour of) premium Hollywood content attracts the point becomes clearer. In turn the Nollywood community get the opportunity to work alongside experienced international professional counterparts — and improve their skills in so doing — whilst still delivering Nigerian cultural stories to new markets in a manner that will drive viewership particularly amongst non-Nigerian audiences.

The third reason for this prediction is the precedent set by the watershed acquisition of Mary Njoku’s ROK Studios by Canal+. Yes, Canal+ is a pay tv business with only a fledgling VOD service. However, Vivendi-owned Canal+’s tentacles spread far and wide, especially in Europe - an extremely competitive market where any advantage in terms of content can have a huge impact on subscriber acquisition/poaching.

Although the post-acquisition strategy will likely focus on deepening the penetration of Nollywood in Francophone Africa, expect some big budget ROK-produced French (and possibly English) language motion pictures for theatrical release. This would break new ground for the growing ROK production team who, til date, have mainly focused on straight-to-TV/VOD content.

3. Increased Genre Diversity — Thrillers, Action, Adventure, Animation

The first reason for this prediction is local, and in particular the saturated nature of the domestic content market for scripted Nollywood comedy and dramas. As can be seen from figures released by the Cinema Exhibitors Association of Nigeria, comedy and drama based Nollywood films make up the bulk of theatrically released content. Whilst solid revenues are still being maintained by these genres, growth in said revenues slowed by over 2%. This possibly indicates that, domestically, the market is looking for different genres and stories asides from (or in addition to) the usual fare.

Regardless of the accuracy of this assertion, one potential factor cannot be overlooked; the Nigeria audience will become increasingly demanding as it grows in consumer sophistication. As the initial novelty attached to cinema culture wanes, the audience will become less and less satisfied with the same storylines (and actors) simply dressed in different clothes. Add that the major allure of the modern cinema experience is the 3D, big screen and surround-sound features which have significantly affected the way today and tomorrow’s film’s are made.

This is even more applicable when one applies it to a western audience (which make up a large/lucrative proportion of a Netflix’s 160m+ subscriber base). Asides from the few million diaspora Nigerians that — possibly for nostalgic and/or cultural connection reasons — are almost certain to watch any Nollywood content that appears on a global VOD platform. Unfortunately, however, they alone are not enough to drive viewing metrics in a manner that would catch the eye on such a platform. This is why it is crucial that Nollywood content begins to appeal to the African-American and Hispanic communities in the US. All that is required is critical mass level of viewership, and the algorithms will take care of the rest. One can therefore expect 2020 will see Nollywood content begin to diversify on a meaningful scale.

The second reason for this prediction is the potential access to global audiences for Nollywood content — something that has only recently become a realistic possibility with the advent of technology as well as the earlier-discussed (slowing) developed market and its rising content costs. It is unlikely that there are currently more than a few hundred thousand subscribers to Netflix (or any other non-local VOD platform) across the entirety of Africa. Thus, the developed markets require fresh (diversified) content whilst the Nollywood is searching for a wider audience. This makes for a mutually beneficial potential relationship. However, rehashed generic Nollywood comedy and drama stories will not gain/keep international audiences used to much more sophisticated content.

This means that well made Nollywood productions in the thriller, horror, action-drama, adventure animation genres will stand out from the crowd of Nigerian content populating the platform. Given that these genres necessitate greater visual and emotional stimulation, Nigerian films in these segments have a stronger chance of attracting wider audiences internationally. Movies such as “Muna”, “King of Boys” and the like spring to mind — the latter having garnered much praise from international critics since its Netflix debut.

The final reason for this prediction is the speed of developments in the Nigerian animated production segment. A country with a large swath of its population under the age of 16 presents significant opportunities for animated stories and characters to be developed with whom this large demographic segment can identify and grow with — not to mention the attendant merchandising and other related opportunities.

Nigeria’s nascent animation industry is full of talent that is now gradually gaining more access to the tools and skills required to thrive in this potentially huge growth segment. Production times in animation are notoriously slow, but technologies are being deployed by leading global animation houses that improve a lot of the bottlenecks, particularly image rendering times. Additionally, the costs of using these advanced studios for the post production/editing work required on high-end animations are extremely inhibiting.

Currently a lot of local animation productions have been in short form (i.e. for web and TV distribution), however 2020 should see Nigerian animation’s first in roads into the feature-length theatrical motion picture space. The successful completion of the Queen Amina novel adaptions, “Malaika”, as well as the successful international licensing of South African produced futuristic African animation series “Mama K’s Team 4” to Netflix, is an indicator of this growing part of Nollywood. The incentives are now greater than ever and Nigerian motion picture animations should begin to make a splash (if not a dent) in the marketplace in 2020.

Conclusion

Nollywood comprises of the cinema, pay tv and VOD segments. Although this post (and its predictions) primarily focused on Nollywood in terms of box office and international VOD distribution, pay tv — although not discussed — is still an important piece of the puzzle. However, the increases in cinema construction, international VOD licensing opportunities, and content production output provide Nollywood with best means of achieving its next wave of growth in the short to medium term.

More funding, bigger budgets, international audience acquisition and expanded revenue streams all point to a blockbuster year and decade ahead for Nollywood.

Let’s hear your predictions.