Reading the Room: Comp Re-Anchoring for African Series B and C Rounds

Three archetype baskets. The discount stack methodology. Six audit questions for portfolio marks

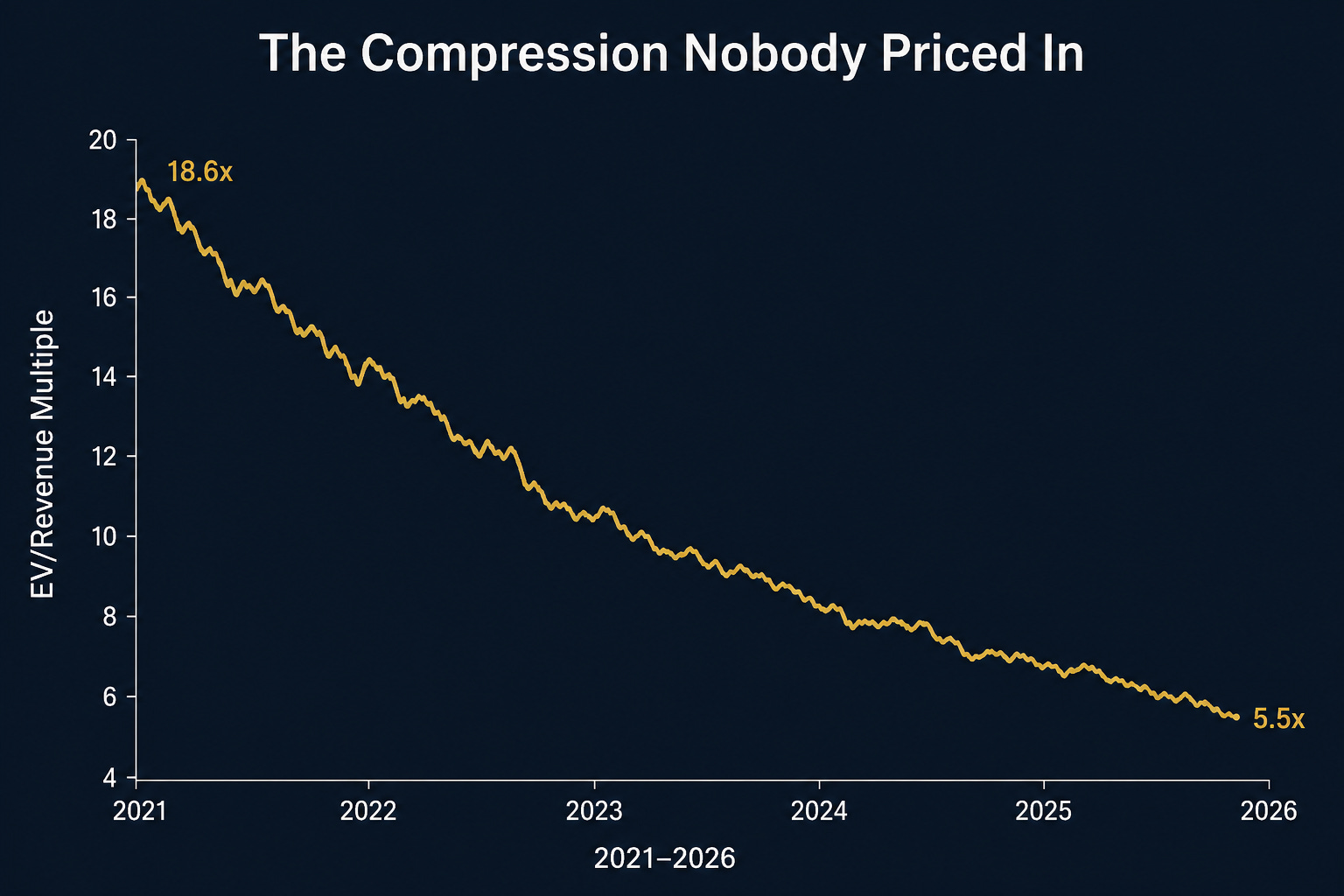

Saturday’s essay made the structural case: African Series B and C rounds are being priced against comp baskets that compressed 70% since 2021, and the same ghost numbers sit inside GP portfolio marks. The reset is mechanical. And the unwind is starting.

This piece is the practitioner version. Three pieces of work, in sequence — the segmented comp baskets that should replace the generic SaaS bundle, the discount stack methodology that converts public comps to defensible private valuations, and the six-question audit checklist for portfolio marks. Worked numerical examples throughout. Practical applications at the end.

The Three Archetype Problem

The most expensive mistake in current African fintech pricing decks is comp-basket conflation. A lending fintech, a payments processor, and an embedded finance B2B SaaS play are three structurally different businesses with three different comp universes. They are routinely priced against the same generic “fintech SaaS” basket.

Archetype 1: The Payments Processor

Payments processors sit on top of payment rails — card processing, mobile money rails, account-to-account transfers, bill payment, agent banking. Revenue is take-rate on transaction volume, typically 0.3% to 1.5% depending on rail and geography. Customer concentration risk is high (top 5 merchants often >40% of revenue). Capital intensity is moderate (settlement float, agent network buildout).

Public comps that work: StoneCo (Brazilian payments, currently 0.5x EV/Revenue, 6.2x EV/EBITDA), PagSeguro (Brazilian payments, similar range), Adyen (European payments premium, currently 8.1x EV/Revenue, 15.2x EV/EBITDA — note Adyen has compressed from 124x EBITDA in 2021 to 15.2x today). The honest comp range for an African payments processor at scale is 0.5x to 4x revenue depending on growth rate, margin profile, and geographic concentration. Above 4x revenue requires Adyen-level margin profile or genuine growth premium that survives diligence.

Important precision: the multiple comparison only works if both companies report on comparable bases. Many African payments fintechs book gross transaction volume as revenue; StoneCo also books gross. Net revenue / take-rate revenue must be compared like-for-like or the multiple becomes meaningless.

Pure software SaaS multiples do not work as comp here. A payments processor with thin take-rate margins is not a high-gross-margin SaaS business and should not be priced as one.

Archetype 2: The Lending Fintech

Lending fintechs underwrite credit — consumer loans, SME working capital, BNPL, salary advance. Revenue is interest income plus fees minus credit losses. Unit economics depend on net interest margin, loss rates, and cost of funds. Capital intensity is high (the loan book is the asset). The model is fundamentally a bank with a tech wrapper, not a software business.

Public comp that works as primary anchor: NuBank (LatAm neobank, currently 4.1x EV/Revenue, $73B market cap on $17B revenue with 29% revenue growth). Secondary comps include Bank Rakyat Indonesia and Tinkoff. Revolut as a private comp anchors at roughly 11.7x EV/Revenue but is not directly verifiable. The honest comp range for an African lending fintech is 2x to 5x revenue — with the upper end requiring NuBank-level customer acquisition economics, NIM discipline, and provable underwriting through a credit cycle.

Note that even NuBank, the global premium neobank by valuation, has compressed materially. Bank of America and UBS cut price targets in early 2026 citing valuation premiums in high-growth fintech contracting. The relevant directional point: the upper end of the lending fintech comp range has moved down, and African lending fintechs priced against pre-2024 NuBank multiples are anchored to comps that no longer exist.

Payments processors do not work as comp for lending fintechs (different unit economics). Pure SaaS does not work either (entirely different capital structure). The most common pricing failure in this archetype is using SaaS multiples on a lending business and ignoring the capital cost of the loan book.

Archetype 3: The Embedded Finance / B2B SaaS Play

Embedded finance and B2B SaaS plays sell software to financial institutions or to non-financial businesses adding financial services — KYC infrastructure, treasury management, payroll, embedded payments APIs, banking-as-a-service. Revenue is subscription plus usage. Margins are SaaS-typical (60-80% gross). Customer concentration is often material (top 10 customers >50% revenue is normal at this stage).

Public comps that work: enterprise SaaS at the relevant Rule of 40 cut. The honest baseline is the current public SaaS median (5.5x revenue Q1 2026) with adjustments for growth rate, retention, and customer concentration. The Rule of 40 filter is the standard discipline — companies below 40 (growth rate + EBITDA margin) trade at substantial discounts to median and should not be comped to median-tier names.

The honest comp range for African embedded finance / B2B SaaS is 3x to 7x revenue with the upper end requiring genuine Rule of 40 performance and customer diversification.

A Note on Hybrid Businesses

Many African scaleups span archetypes — Flutterwave is payments + lending + B2B SaaS; Wave is payments + remittance; Paystack-now-Stripe-Africa is payments + embedded finance. For hybrid businesses, the comp basket should be a weighted average across archetypes by revenue contribution. A 60% payments / 40% B2B SaaS business at $30M revenue should be comped at roughly (0.6 × 2.5x payments) + (0.4 × 5.5x SaaS) = 3.7x effective revenue multiple before discount stack. The weighted approach prevents the most common hybrid pricing failure, which is comping the entire business at the higher-multiple archetype.

The Discount Stack Methodology

Raw public comps are only the start. The discount stack converts public to private to African to FX-adjusted. Most decks apply discounts that are too small individually and stack them in the wrong order.