The Founder Power Curve: Why Building a Camel Doesn’t Make You Sellable

Operating excellence is one problem. Transferability is another. Most African founders only learn the difference during diligence

Building a camel is table stakes. But that alone does not make you sellable.

The same operating discipline that produces a sustainable African company can produce a company no PE buyer can transact on. Operating excellence is one problem. Transferability is another. Both are required for a founder outcome, and they sit in sequence — the second only matters once the first is solved. Most founders who have correctly internalised the camel model will still lose their exit at the transferability layer. They lose it because the legal scaffolding around the business makes the sale impossible, not because the business itself failed.

Twelve weeks ago, in The Camel Imperative, I argued that Africa’s next winners won’t be unicorns. They’ll be companies built on five principles: cash conversion before growth, positive unit economics at the transaction level, FX-hedged revenue architecture, local cost discipline, and exit optionality designed for the regional banks, telcos, and corporates buying at $30–80M. That argument has held. The buyer class that essay named is now the dominant exit pathway. AVCA’s 2025 data confirmed sponsor-to-sponsor transactions reached a record 26% of African PE volume — which means PE firms are increasingly buying from other PE firms, not from founders. The reason matters, and it gets to what the Camel essay didn’t address.

The Window Is Closing Faster Than Founders Realise

The DPI wall is now in front of GPs holding 2019–2022 vintage Series A positions across the continent. Those funds need exits in the next 18 to 36 months or they face fundraising collapse on their next vehicle. That timing pressure transmits directly to portfolio companies. Founders in those portfolios will be pushed toward sale conversations whether they’re ready or not, because the GP’s survival depends on it.

The push is happening into a buyer class with diligence requirements that strategic acquirers do not impose. Strategic buyers absorb operational mess because they’re buying capability, market position, or talent. They can integrate, restructure, and write down what doesn’t fit. PE buyers operate under a different constraint. They’re buying a financial asset that needs to operate, grow, and re-sell within a defined hold period. Every defect they inherit becomes their problem to solve before their own exit, which means they price defects in or walk away.

The decisions that determine whether you carry defects into a sale process are made at Series A. By Series B those decisions are largely locked. By the time exit-readiness becomes urgent, they cost equity, time, and sometimes the deal itself to remediate. The founder who learns this during diligence learns it too late.

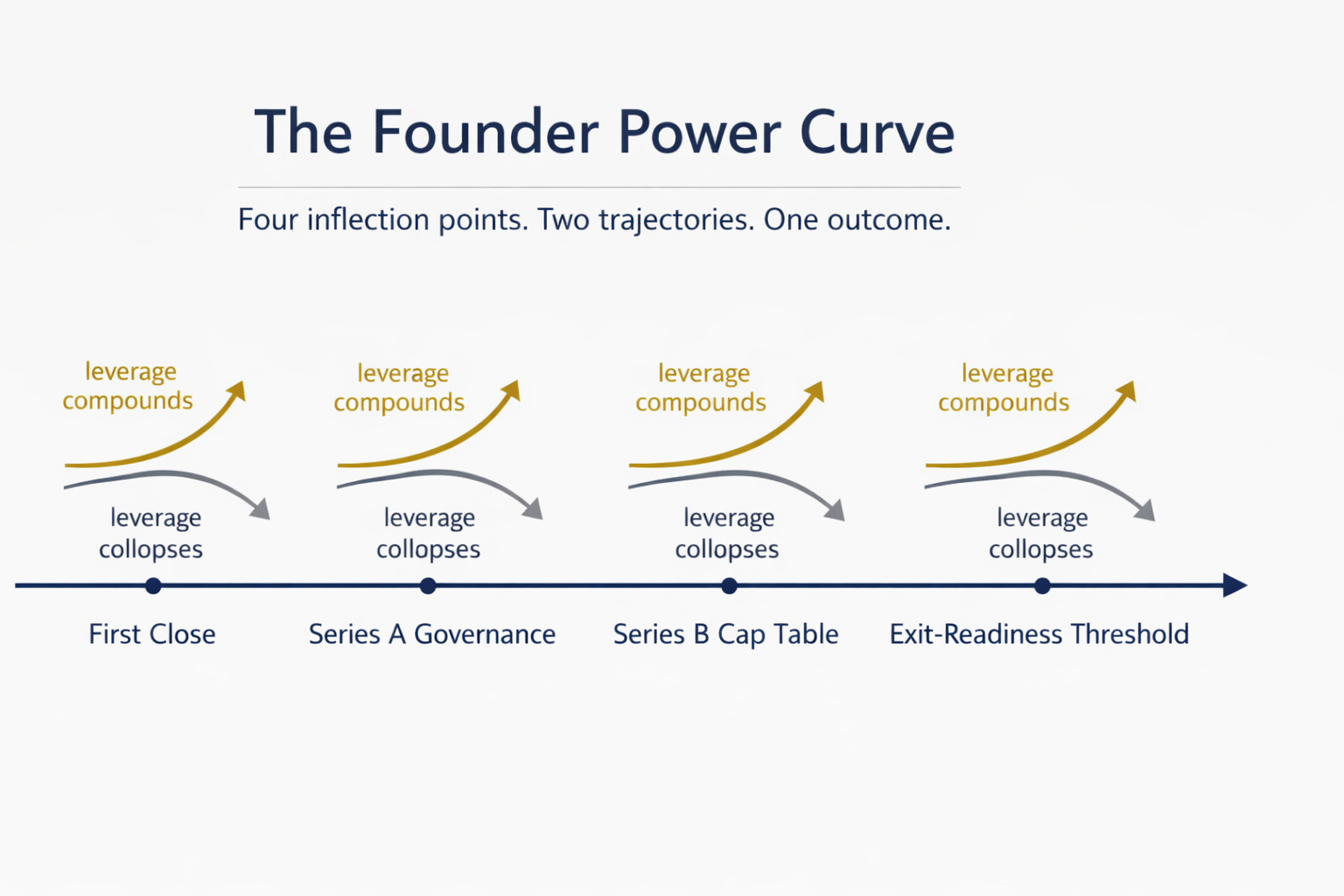

The Founder Power Curve

Four inflection points map where founder leverage compounds or collapses. At each point, a specific decision category determines whether the company becomes more sellable or less.

Inflection Point 1 — First Close. The decisions made here look small and are not. Cap table architecture from day one matters more than founders typically appreciate: a single share class for founders, vesting schedules with cliff and acceleration provisions, founder employment agreements with IP assignment that survives termination. The opposite trajectory is recognisable in retrospect. Stacked convertible instruments — SAFEs and bridge notes layered over multiple closings, post-priced-round side-letters to specific investors, conversion mechanics never cleanly executed across jurisdictions — surface during diligence as a forensic exercise nobody wants to fund. Informal equity grants made to early collaborators without documentation. Intellectual property held in personal name, or worse, jointly with a co-founder who later left. PE diligence will find every uncleaned instrument. Each one becomes either a price discount or a deal-killer, depending on how aggressive the buyer is and how exposed the seller is to time pressure. Most First Close defects can be remediated cleanly at Series A if caught early. By Series B, remediation costs equity, time, and sometimes the deal.

Inflection Point 2 — Series A Governance. What compounds leverage here is building a real board. Independent directors where appropriate. Formal board resolutions for material decisions. Written delegation of authority. Audited financials from year one. Related-party transaction protocols documented and enforced. What collapses leverage is the founder-controlled board with passive observer rights for investors, decisions documented in WhatsApp threads, commingled accounts with founder-owned entities, and no audit trail for material changes in capitalisation or strategy. PE buyers cannot transact on a company whose decision-making history is undocumented. They cannot defend their investment committee approval without that documentation. Post-LOI becomes governance reconstruction work, and reconstructed governance never reads as cleanly as governance built in real time.

Inflection Point 3 — Series B Cap Table. Protective provisions calibrated to investor stage, drag-along rights with reasonable thresholds, ROFR and co-sale terms structured to permit secondary liquidity without blocking primary exits, anti-dilution that doesn’t trigger a death spiral in a down round. The collapse trajectory is more common than founders admit. Stacked liquidation preferences that mean founders earn nothing below a high exit threshold. Veto rights distributed across too many investors creating exit blocking. Protective provisions written in early-stage shorthand that don’t scale to growth-stage deals. The cap table determines whether the deal closes at all. A buyer can love the business and walk away when waterfall mechanics make the founder mathematically indifferent to closing — because a founder with no economic upside has no incentive to navigate the deal through to completion.

Inflection Point 4 — Exit-Readiness Threshold. This is where the prior three points either pay off or fail to. The compound-leverage decisions: 18 to 24 months of audited financials available on demand, customer contracts with clean assignment provisions, employment agreements with non-competes and IP assignments that survive termination, regulatory licences held in the operating entity rather than scattered across subsidiaries, a data room maintained continuously rather than built reactively. The collapse decisions are the mirror image. Financials reconstructed from bank statements during diligence. Customer contracts that terminate on change of control. Key employees on handshake deals with no formal employment terms. Licences held in the wrong entity or in personal capacity. Data room thrown together in 60 days under exclusivity. Every gap surfaced during diligence either reduces valuation or kills the deal. In distressed exit conditions — which is what most African Series B exits will be in the next 24 months — both outcomes get worse, because the seller has lost the leverage to push back on buyer demands.

The curve compounds. Each inflection point’s decisions either remediate prior gaps or stack on top of them. Founders who get Point 1 right have a meaningfully easier path through Points 2 and 3. Founders who get Point 1 wrong spend Series A and B capital on remediation work that should have been part of the original build — and that capital is not coming back, regardless of how the exit ultimately resolves.

What the Numbers Look Like

Three pieces of evidence ground the framework.

The first is in the AVCA 2025 sponsor-to-sponsor data. PE firms buying from other PE firms now represent 26% of African PE deal volume, a record. The implication that doesn’t get discussed enough: PE buyers are increasingly buying from other PE sellers because those companies have been cleaned up by the selling fund’s portfolio operations team. Founder-led companies arriving at the PE buyer class directly face a meaningfully higher diligence standard than secondary PE assets, precisely because they haven’t been pre-cleaned by an institutional seller. That disadvantage isn’t visible to founders until they’re inside diligence, at which point it’s too late to address without conceding price.

The second is what the transferability layer is worth in valuation terms. Consider an illustrative scenario based on patterns observable in recent African fintech transactions. Two Series B companies, both at roughly $8M ARR, both growing 60% year-over-year, both EBITDA-positive. Company A has clean governance, audited financials going back three years, single jurisdiction of incorporation, IP cleanly held in the operating entity, and a standard four-class cap table. Company B has the same operating metrics, but commingled accounts that were partially separated last year, IP still held partly in the founder’s personal name, three jurisdictions across operating subsidiaries, and four classes of preferred with stacked liquidation preferences from successive down-rounds. Same business at the operating level. Company A transacts in the 4–5x revenue range commonly observed in clean African fintech sales. Company B transacts in the 2–3x range — if it transacts at all. The transferability layer is worth 40–50% of enterprise value at exit, and that spread shows up nowhere in the operating financials. It’s purely a function of how the company is wrapped.

The third piece of evidence is where most African PE deals actually die. Not in valuation negotiations or commercial terms, but in contract review. Customer contracts, employment agreements, and supplier arrangements containing change-of-control provisions written by local counsel without exit-readiness in mind. Customer contracts carry the most weight here, because they underpin the valuation itself — particularly key enterprise contracts that account for a meaningful share of total revenues. The buyer cannot assume the contracts as drafted. The seller renegotiates them under time pressure during exclusivity, often with counterparties who realise their leverage and extract concessions. I have seen this kill multiple transactions over the last few years, and in every case the underlying drafting failure was preventable at the point of original negotiation, sometimes years earlier. This is the practitioner judgment layer in action — contract drafting that anticipates exit at the point of negotiation, rather than discovering during diligence that the wording doesn’t support a sale.

The Three-Test Gate

Three tests determine whether you are in the PE-addressable universe at all.

The first is governance legibility. Can a third-party diligence team reconstruct your decision-making history from documents alone, in 90 days? If material decisions live in WhatsApp threads, founder memory, or undocumented agreements, the answer is no. The deal cannot proceed without governance reconstruction work that no PE buyer wants to fund.

The second is cap table cleanliness. Can a buyer model the waterfall in 30 minutes and confirm that founder, management, and key investors are all economically aligned to close at a target valuation? If the waterfall requires a specialist to model, or if the alignment math reveals that the founder earns nothing meaningful below a high threshold, the deal stalls before terms are even negotiated.

The third is structural transferability. Can the operating entity be sold without consent friction from contracts, regulators, jurisdictions, or minority holders? If the answer requires a renegotiation campaign with third parties before close, the buyer either prices in the friction or walks.

Companies that pass all three are the addressable universe for the emerging PE buyer class. Companies that fail any one are not in that universe. They may still reach a strategic acquirer exit, which has a different and longer-tail buyer pool. They may exit through a secondary sale (albeit likely at meaningful discount). Or they may not exit at all. The point isn’t that any of these is automatically wrong — a strategic exit at the right multiple is a real outcome. A secondary in which a founder sees liquidity is still liquidity. The point is that founders should know which exit pathway they are actually building toward (if any), rather than discovering it when the GP starts pushing for a sale process they aren’t structured to support.

This is not a product problem or a market problem. It’s simply a preparation problem. The decisions that determine whether you pass the three-test gate are inexpensive to get right at Series A — the marginal cost of doing the work properly versus doing it cheaply is small. By Series B you’re paying to remediate on top of new work. By exit-readiness you’re paying with deal economics, or the deal itself. Operating discipline keeps the company alive long enough for an exit to be possible. Without the transferability layer, that exit doesn’t happen.

What Comes Next

The three-test gate is the qualifying filter. The clause-level architecture that determines whether you pass each test is where most founders need practitioner judgment they don’t have in-house — because local counsel drafts for the round in front of you, not for the exit two rounds away. Midweek piece, The PE-Readiness Diagnostic, walks through the specific governance, cap table, and contract criteria PE acquirers apply to African founder-led companies, and where the most common failure modes sit. Paid subscribers get the full diagnostic. Free subscribers get the framework summary.

The window for getting these decisions right is the 12 to 24 months before your GP starts the conversation you didn’t know was coming. Most founders find out the hard way. The ones who don’t, build for it deliberately.

Insightful and practical. Thank you for sharing.