READING THE ROOM

A GP’s Field Guide to Fundraising in a Broken Liquidity Cycle

The free essay last Saturday named the problem. This piece is about what to do with it.

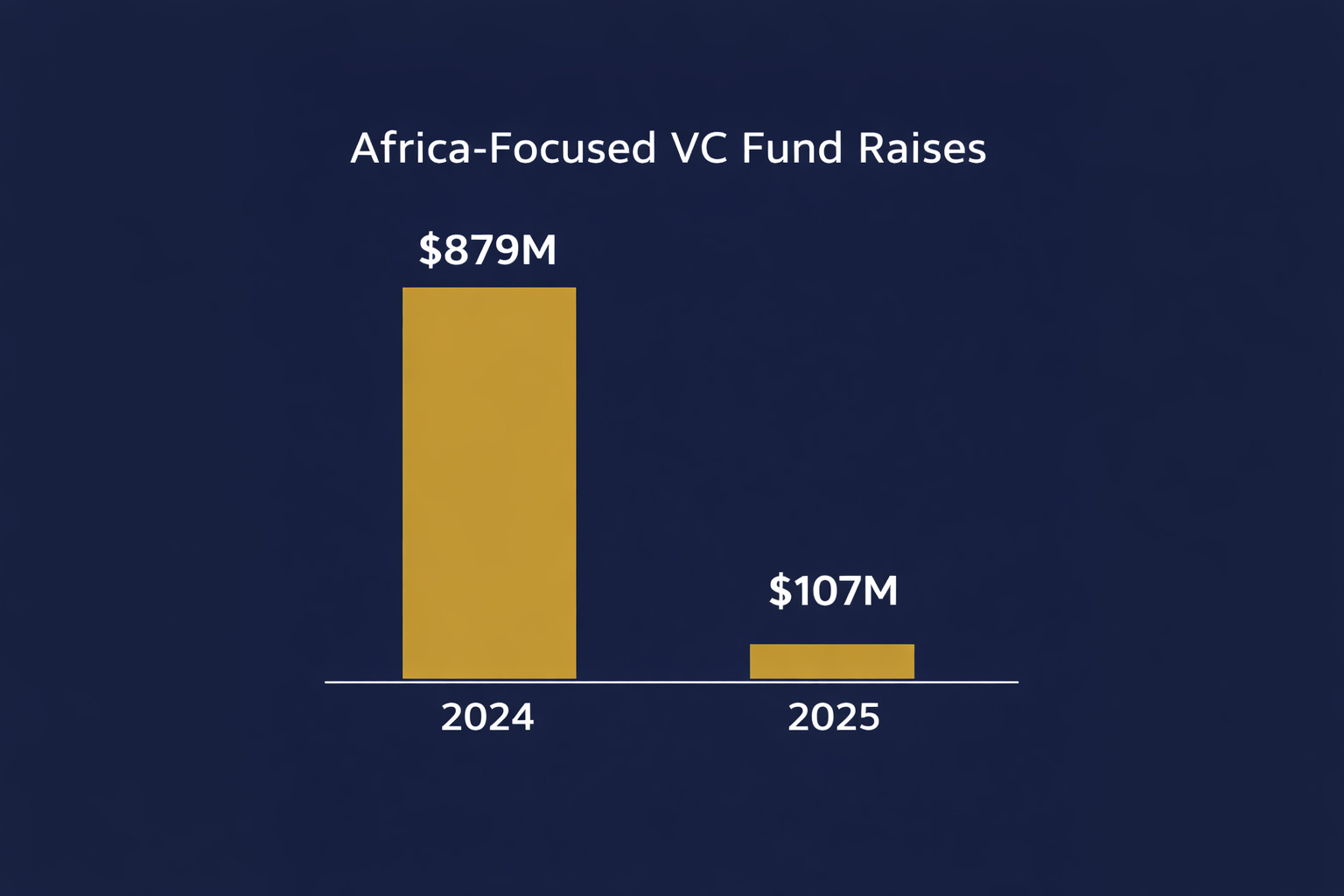

If you’re in fund formation right now — or planning to be in the next twelve months — the 87% collapse in Africa-focused VC fundraising is the operating environment, not background noise. The LP pools that funded your last vehicle have materially contracted. The geopolitical conditions that supported DFI risk appetite have deteriorated. The Iran war has added a fresh psychology shock to an already stressed market.

None of that changes because you have a strong track record or a differentiated thesis. What changes is who you pitch, how you pitch them, and when you realistically expect to close.

Three Questions Worth Thinking About

Which LP pool are you actually targeting?

Most GPs entering conversations right now are working from a 2022–2023 map of the LP landscape. That map is wrong.

European private institutional capital fell from 70% of Africa-focused fund commitments to 21% in a single year. Global DFIs are redirecting mandates toward climate finance and energy transition — a shift driven by EU policy frameworks, not a temporary pause. Gulf family offices are focused on domestic security and post-war reconstruction spending. These pullbacks have different causes but the same practical effect: the capital that anchored most fund closes between 2019 and 2023 is no longer in the room.

What remains is more fragmented and harder to read. African corporates stepped up sharply — 41% of 2025 commitments, from 7% in prior years. African DFIs with localised mandates are increasingly willing to anchor domestically managed vehicles. North American impact capital has been more stable than European, though at lower volumes and with tighter sector requirements.

The pitch for an African corporate LP is a different conversation from a DFI. Different timeline, different diligence questions, different expectations around board representation and reporting. If you’re running one deck across all audiences, you’re not optimised for any of them.

What is your vintage framing?

Every LP you meet right now is sitting with the same unspoken question: why raise into this?

The answer is in the data, but most GPs aren’t leading with it (I see a lot of decks). Funds raised during periods of LP risk-off and compressed valuations historically outperform. The J-curve looks better when entry prices are low and the deployment window coincides with recovery conditions. A fund closing in late 2026 or early 2027 deploys into 2027–2029 — potentially among the stronger entry vintages of the decade.

The valuation evidence is there. Capital in 2025 concentrated into fewer, more mature companies — median deal sizes rose 32% year-on-year as the distribution narrowed. Early-stage pricing compressed. A fund deploying now enters positions that would have cost meaningfully more at 2021 pricing. If the global liquidity cycle turns — and historical Fed tightening cycles suggest a turn 18–30 months after peak rates — the vintage advantage compounds on exit.

Don’t let the LP discover this argument halfway through diligence. Lead with it.

This post is for paid subscribers.