The PE-Readiness Diagnostic: The Three Tests That Determine Whether You’re Sellable

The clause-level architecture behind governance legibility, cap table cleanliness, and structural transferability — and where most African founder-led companies fail.

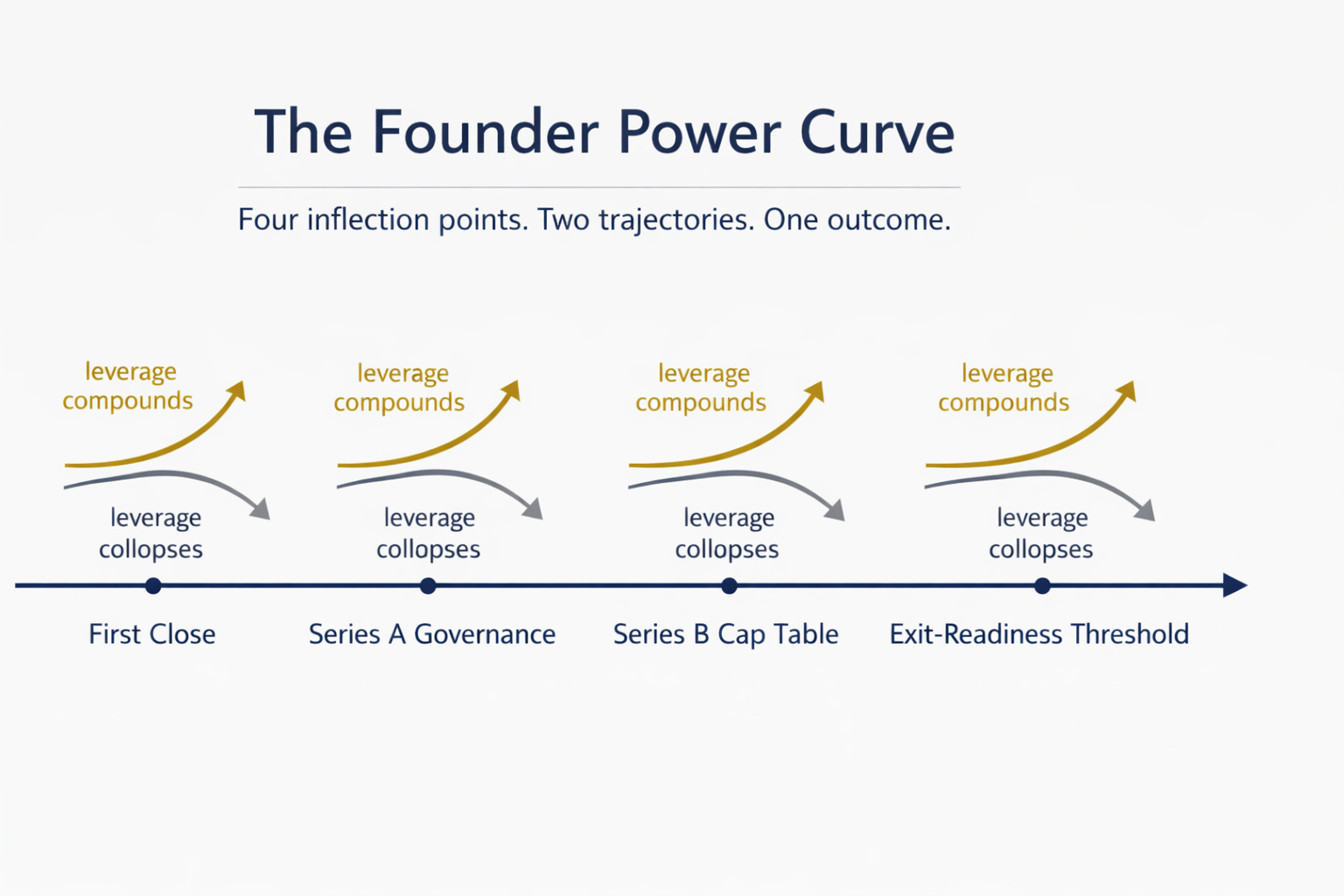

Saturday’s essay named the Founder Power Curve and ended with three tests: governance legibility, cap table cleanliness, and structural transferability. Pass all three and you are in the PE-addressable universe with negotiating leverage. Fail any one and the buyer either prices the friction into the deal or walks. The framework does the diagnostic work. What it does not do is tell you the clause-level architecture behind each test — the specific provisions, thresholds, and contract language that determine which side of the gate your company actually sits on.

The DPI wall is now in front of GPs holding 2019–2022 vintage Series A positions across the continent. Those funds need exits in the next 18 to 36 months. Portfolio companies in those funds will be pushed into sale conversations whether they are ready or not, because the GP’s survival depends on it. The companies that pass the three-test gate will transact at clean multiples. The companies that fail at least one test will transact at meaningful discount, transact through a longer-tail strategic acquirer pathway at lower price ceilings, or will not transact at all.

What follows is the clause-level architecture for each test — the specific provisions, thresholds, and contract language that determine which side of the gate your company actually sits on. The order matters. Governance legibility is the threshold gate. Cap table cleanliness determines whether the deal can close economically. Structural transferability determines whether the deal can close mechanically. Each test has its own failure modes, its own remediation costs, and its own window for being addressed.

Test 1 — Governance Legibility

The diagnostic question: can a third-party diligence team reconstruct your company’s decision-making history from documents alone, in 90 days?

If material decisions live in WhatsApp threads, founder memory, or undocumented side agreements with early investors, the answer is no. Every PE buyer’s investment committee requires documentary evidence of how the company has been run. The absence of that evidence is not something the buyer can fix after acquisition. It becomes governance reconstruction work that no PE buyer wants to fund, and the deal cannot proceed until it is done.

What compounds leverage at Series A:

Board composition. At least one independent director by Series A close. Formal nominating mechanics documented in the shareholders’ agreement. Board observer rights distinguished in writing from voting rights — a common failure mode is investors with observer seats who have accumulated informal decision-making influence that creates diligence ambiguity about who actually has authority.

Resolution discipline. All material decisions captured in written board resolutions, signed and dated. Material means capital raises, M&A activity, key hires above a defined compensation threshold (typically $150K or the local equivalent), related-party transactions of any size, and strategic pivots affecting the capital plan. Decisions below the threshold can live in management approvals; decisions above it need resolutions. The diligence test is whether a stranger reading the minutes understands why the company is where it is.

Audit infrastructure. Big Four or top-tier local equivalent audit engagement by Series A close. Clean opinion required. Qualified opinions are not automatic deal-killers at Series A, but they are at Series B and at exit. Audit firm changes mid-cycle without disclosed rationale create red flags that diligence teams will pursue — if you change auditors, document the reason contemporaneously.

Related-party transaction protocols. Written policy, pre-approval mechanics, separate signing authority for any transaction involving founder-affiliated entities, family members, or entities in which directors hold material interest. Commingled accounts between the operating entity and founder-owned vehicles are the single most common Series A governance failure, and they are almost impossible to clean up retroactively in a way that survives PE diligence.

Common failure modes and their consequences:

Founder-controlled board with passive observer rights for investors. Cannot survive PE diligence. Remediation requires investor consent to restructure, which is difficult when the founder is negotiating from a weaker position than they held at the original round.

Decisions documented retroactively when diligence demands it. Reconstructed governance never reads as cleanly as governance built in real time; diligence teams can tell the difference, and they price accordingly.

Board minutes that capture decisions but not rationale. A diligence team reading minutes needs to understand not just what was decided but why — without rationale, the documentation fails the reconstruction test.

Remediation cost by stage:

At Series A: $15,000–$40,000 in legal and audit scoping work. Most Series A governance issues are cleanable if addressed at the round itself.

At Series B: $80,000–$150,000 and four to six months of structured remediation work. Requires investor consent for material changes.

At exit: deal economics. Governance reconstruction during exclusivity gives the buyer leverage to extract price concessions or walk away entirely.