The Private Credit Money Is Showing Up. But It’s Underwriting the Wrong Thing

Nigerian FMCG balance sheets are becoming distributor banks by accident. African private credit is queuing to underwrite the wrong asset class

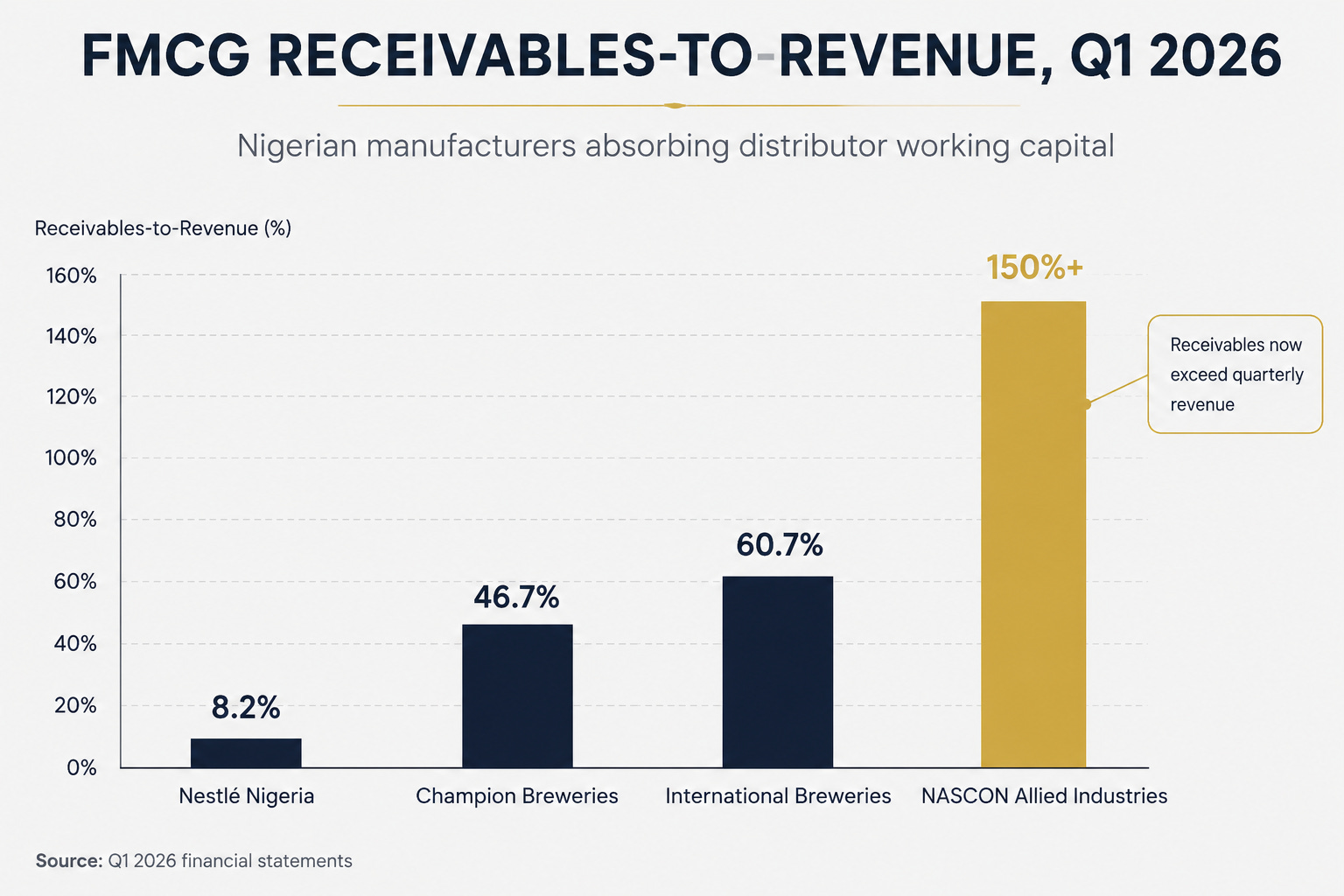

NASCON Allied Industries — the salt and seasoning manufacturer that anchors much of Nigerian household cooking — closed Q1 2026 with receivables sitting at more than 150% of its quarterly revenue. Read that number twice. NASCON is profitable, well-capitalised, part of one of Nigeria’s largest manufacturing groups. International Breweries, owned by AB InBev, is sitting at 60.7%. Champion Breweries at 46.7%. As I’m watching this from a buyer-side seat, what’s interesting isn’t that the receivables grew. It’s why, and what it says about where the working capital in the Nigerian economy is actually being warehoused.

The bank balance sheets that used to fund distributor working capital are paying down hard. FMCG firms collectively repaid roughly ₦1.2 trillion of debt across 2025. Nestlé Nigeria alone cut borrowings from ₦653 billion to ₦476 billion. Meanwhile the new capital rotating into African credit markets — TLG Capital’s $200 million Africa Growth Impact Fund, FCMB Asset Management’s pension-funded private debt vehicle, the AVCA-reported $2 billion private debt pipeline set to deploy by 2027 — is being directed predominantly into corporate term loans, mezzanine, and growth equity. The receivable piling up on Nestlé’s balance sheet has no institutional buyer at scale because the underwriting capability for it was never built locally at sufficient scale.

The Nestoil syndicate impairment essay two weeks ago named the supply-side of this story — Nigerian banks reallocating away from corporate underwriting after absorbing roughly ₦3.2 trillion in oil and gas-linked losses. This piece names the demand-side mirror. What happens to the asset classes a market can’t underwrite, once the capability for the wrong one has consumed all the available capital.

The Working Capital Migrated. Nobody Marked Where It Went

Through 2023 and 2024, naira reforms and monetary tightening repriced bank corporate credit violently. The monetary policy rate — MPR, what banks pay to borrow from the central bank — climbed past 27%. The cash reserve ratio sat at 50%, meaning banks had to keep half of deposits sterilised at the central bank rather than lending them out. FMCG companies with FX-denominated debt absorbed severe finance cost hits. Servicing those debt stacks was destroying earnings faster than operations could compensate, so in 2025 the deleveraging began.

Two different bank lending books are shrinking simultaneously and for different reasons. The ₦1.2 trillion repaid by FMCG manufacturers is corporate debt the manufacturers themselves took on for capex, FX hedging, and balance sheet purposes. That book shrank because the interest cost became unbearable. A separate book — working capital loans to distributors — is also shrinking. The second book is the one this essay’s argument hinges on.

The demand side never recovered with the deleveraging. Nigeria’s Purchasing Managers’ Index — PMI, the headline forward indicator of business activity — slipped to 49.4 in April 2026, the first contraction reading after sixteen consecutive months of expansion. Distributors who used to pay upfront for inventory cannot. The choice manufacturers face is ugly and simple. Tighten credit to distributors and watch volumes collapse. Or extend it and absorb the working capital onto their own balance sheet. They’ve chosen the second.

Follow the cash through three parties. Nestlé manufactures and ships to a distributor — a mid-sized business that buys in bulk and resells to thousands of retailers across a region. The distributor collects from retailers over 30 to 60 days. Until recently, the distributor bridged that gap with a working capital loan from a bank — First Bank’s FMCG Key Distributorship Finance is one example. Nestlé got paid in 14 days. The bank earned interest on the bridge. Everyone’s economics worked.

What broke is the middle link. With MPR above 27% and naira lending rates following, the working capital loan that used to cost the distributor around 20% now costs 30–35% — beyond what FMCG distribution margins can absorb. Distributors asked the manufacturers for longer payment terms. To defend volume, the manufacturers said yes. Now Nestlé ships on day 1 and collects on day 60. For those 60 days, Nestlé is performing much of the credit function the bank used to perform — without the underwriting tooling and without explicit pricing of the balance sheet burden it has absorbed.

The receivable hasn’t disappeared. It has migrated from one balance sheet to another. Before, it sat as a loan asset on the bank’s books, with the distributor carrying it as a liability. Now the bank’s loan book has neither side of that entry, the distributor’s borrowing line is smaller, and Nestlé carries a large trade receivable on its own balance sheet. The migration is economically inefficient on its new home because Nestlé is holding working capital at its full cost of capital and earning nothing for it directly. A credit specialist holding the same receivable would carry it at a lower cost of capital and get paid a spread for performing the function. Nestlé pays the holding cost primarily to preserve distribution continuity and volume; a specialist pays a smaller holding cost and earns an explicit return for warehousing the risk itself. The asymmetry is the whole point.

NASCON’s 150%-of-revenue receivables ratio is the visible expression of that migration. International Breweries and Champion confirm it as a pattern. A skeptical reader could argue the receivables growth reflects benign factors — strategic payment-term extensions, accounting policy changes, revenue mix shifts. The simultaneous PMI contraction, sector-wide debt repayment, and named-firm consistency make the distress interpretation the better one. The squeeze is real; it just hasn’t fully translated into reported impairment yet. The Camel logic this publication has worked through before applies in reverse here — capital-efficient design is what manufacturers thought they were building when they deleveraged. Instead they’ve absorbed the kind of balance sheet risk the framework warns against, because no credit specialist was available to take it at workable pricing.

Private Credit Came to Africa. It Brought the Wrong Playbook

The new private credit capital arriving in Africa is good news. It is also, predominantly, the wrong product for the gap that actually exists. Three reasons, all observable from fund mechanics themselves.

Ticket size first. A $200 million fund needs to deploy in $5–20 million tickets to keep diligence costs proportionate and portfolio concentration manageable. Receivables financing structures clear at $500,000 to $5 million per facility in this market. The math doesn’t work for the fund’s GP economics, so the fund pushes upmarket into corporate term loans where it can write cheques that justify the diligence cost.

Tenor is the second mismatch. TLG’s stated product offers seven-year tenors with three-year grace periods. That’s growth capital. Receivables financing is 30 to 120-day revolving credit, with the borrowing base — the pool of eligible receivables backing the facility — recalculated continuously. A fund designed for one cannot pivot to the other mid-life.

The third reason runs deeper. Receivables underwriting requires assessing the buyer of the receivable — the FMCG manufacturer or telco offtaker who owes the money — rather than the seller who is borrowing against it. African credit markets, both bank and private, have spent decades building underwriting capability for sponsor-cashflow risk — the same capability that produced Nestoil and the ₦3.2 trillion of bank impairment that followed. The asset-class-specific capability for receivables — whether trade, contract, or IP-linked — has not been built at scale. With limited exceptions worth naming.

Afreximbank has been promoting factoring across the continent for over a decade. South Africa hosts most of the developed factoring volume. The Nigerian SEC’s 2025 rules on private debt issuance opened a regulated channel for receivables-backed instruments. Bibby Financial Services launched an Africa platform. None of this is invisible. It just hasn’t reached the scale that would absorb the receivable volume now sitting on FMCG balance sheets.

OmniPay — the financial arm of the OmniRetail B2B distribution platform — reportedly processes around $95 million in monthly transaction volume, extends credit at roughly $4 million monthly against the same receivable universe, and reports default rates below 1%. Set those numbers against TradeDepot’s $110 million raise anchored on BNPL for five million SMEs, and Alerzo’s 2021 lending product — both reportedly suffered significant losses on credit and paused programs to regroup. Same retailers. Same receivables. Same macro environment. Radically different default outcomes.

Almost nobody outside operating B2B circles is reading this gap as a credit signal. The most plausible structural explanation is the underwriting architecture itself. OmniPay sees transaction flow on its own platform, documents receivable ageing in real time, and underwrites the offtaker risk — Tolaram’s MultiPro subsidiary, which moves through OmniRetail’s distribution — rather than the retailer-as-borrower risk the failed lending programs were chasing. The distinction between underwriting the credit of the entity buying the goods versus the entity selling them remains the architectural difference the rest of the market is missing.

The Underwriting Is Knowable. The Talent Isn’t

A receivables facility is straightforward at the core. Somebody buys the right to collect a future payment. Advances most of the cash now. Absorbs the risk that the payment comes in late or short. Everything else is architectural detail around that core trade.

Applied to the FMCG case, Nestlé — not the distributor — becomes the originator. Nestlé sells its trade receivables to a specialty credit fund at a discount to face value, gets cash on day 1, and the fund collects from the distributor on day 60 and earns the discount as its return. Nestlé’s balance sheet returns to the old shape — cash, not receivables. The credit function moves to a specialist whose cost of capital is lower than Nestlé’s and who gets paid for performing it. The same architecture applied to a music catalog works in the same direction — the artist or label sells its forward royalty receivables to a specialist who advances cash today and collects from the streaming platforms and PROs over the licensing tail. Different asset class, same structural move.

Advance rates typically run 70–85% of eligible receivable face value, depending on debtor concentration, dilution experience, and obligor credit quality. A dilution reserve absorbs returns, allowances, and disputed invoices. Concentration limits cap exposure per debtor and per industry. Pricing builds off MPR plus a spread that reflects underwriting capability and operational cost rather than equity-style risk premium. Currency exposure is layered carefully — naira receivables funded with naira capital, FX overlay only where the underlying receivable is export-linked.

Priced correctly, this structure generates 18–24% naira returns on an asset with verifiable cash flow performance. The OmniPay default experience — sub-1% against $4 million monthly deployment — shows what the asset class can achieve when underwritten properly. That’s a better risk-adjusted return than the corporate term-loan paper the private credit funds are buying, if the underwriting and servicing infrastructure exists to capture it.

Where structures fail in practice is at four specific points. How eligibility is defined — does a delivered-but-disputed invoice count, and under what cure terms? How dilution is reserved. How perfection of security is established under Nigerian law, against the backdrop of the Secured Transactions in Movable Assets Act and the National Collateral Registry — and how assignment is notified to the underlying obligor to defeat set-off and netting risk if the distributor pays the wrong party in ignorance. And how cash trap mechanics actually operate when payment is deferred — who controls the collection account, what triggers a sweep, how the waterfall runs when receivables come in late or short. Each is solvable. None is solved by capital arriving.

The Underwriting Talent Question Is the Deeper Story

The Nestoil essay named that Nigerian bank corporate-underwriting capacity is reallocating. This essay names what the new capital is walking past on its way to replacing what’s reallocating away. The reallocation question isn’t only where the bank capacity goes — it’s what the next generation of African private credit chooses to underwrite, and whether that choice differs in kind from what the banks were doing before. On the current trajectory, it largely doesn’t.

The African VC DPI gap — distributions to paid-in capital, the cash returned to investors after fund fees — and the African private credit underwriting gap are likely related phenomena. Pattern observation more than proven mechanism, but consistent across enough asset classes to be worth naming. Capital deployment is outpacing the development of asset-class-specific underwriting capability. Whether the asset is a software company’s exit multiple, a music catalog’s streaming royalty stream, or a distributor’s receivable book, the question is identical. Who has built the capability to value this thing properly, and what happens when the capital arrives before the capability does? Both markets are answering that question in real time. The answer matters for which capital pools end up profitable a decade from now — and for the founders, artists, and operators whose assets are being valued by buyers who may or may not know how to value them.

I see this from two sides — corporate buyer-side underwriting on one, IP and contract receivables on the other. The pattern is the same. The asset class itself doesn’t matter as much as whether the institutional capability exists to value it.

What This Means

The private credit narrative being told about Africa right now is a capital-supply story. The data supports a different one — an underwriting-capability story. Capital is necessary but not sufficient. The funds, advisors, and operators who will produce real returns from African capital markets over the next decade won’t be the ones that arrived with the biggest cheques. They’ll be the ones that built — or hired, or partnered for — the specific capability to value the asset classes the continent actually generates in volume.

This question runs wider than credit. Anyone deploying capital, time, or attention against an asset whose value isn’t yet legible faces the same problem. The artist whose catalog earnings are growing but whose label can’t structure against them. The founder whose unit economics are real but whose investors can’t price what comes after profitability. The CFO watching receivables accumulate that no bank will fund at workable terms. Each is a different version of the same gap.

Nestlé doesn’t want to be a bank to its distributors. The receivable will eventually be warehoused, financed, and priced by somebody. The question is whether that somebody is a Nigerian institution that built the capability locally, or a foreign specialty fund that priced in the capability shortage as a risk premium and clipped the spread for itself.

A short note before I close. The next L.U.M.I. Brief lands Saturday 6 June. I’ll be in Mecca for Hajj for the two weeks between. The next piece will pick up where this one ends — the same architectural question applied to music IP specifically. Catalog earnings sitting on artist, label, and manager balance sheets the way these receivables are sitting on Nestlé’s — visible to anyone who looks, unstructured at scale because the capability hasn’t been built. I’ll write that one when I’m back.

Until then, the data this essay rests on is public. NASCON’s receivables ratio is in their Q1 statement. The OmniPay figures have been reported. The FMCG deleveraging is in audited filings. Pick any one of those threads and pull on it. The structural picture this essay names becomes more visible the closer you look at any single piece of it.

— Lumi

insightful piece, done my first read— will re-read for extra insights and context.

Thanks for doing the work and wishing you a fruitful Hajj. Allah Rahman.