The 45% Mirage

Africa’s venture capital is raising more from domestic investors than ever. The problem is which domestic investors.

The question worth asking about Africa’s 2025 venture capital numbers isn’t how much was raised. It’s who, exactly, is now being counted as a domestic investor.

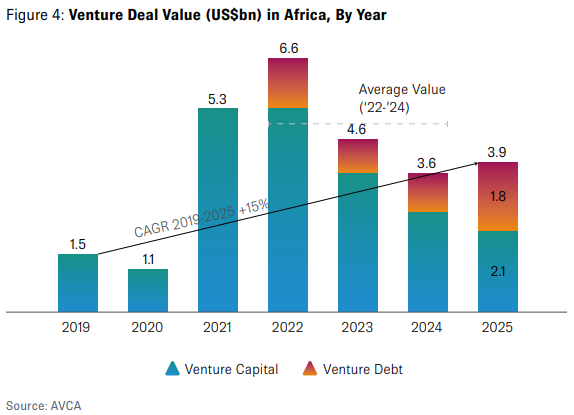

AVCA’s seventh annual Venture Capital Activity in Africa report, released earlier this month, puts the headline figures on the table. African startups raised $3.9 billion last year across 506 deals — a figure Partech Africa’s concurrent annual report rounds slightly higher at $4.1 billion once all debt instruments are captured. Africa was the only global region where venture deal activity didn’t decline. Domestic investors hit a record 45% of venture fund commitments, nearly double their 23% average from 2022–24. AVCA’s CEO described the shift as a “recalibration towards patient, structured and locally anchored capital.” The narrative writes itself: Africa’s ecosystem is finally anchoring to homegrown capital.

Look closer and the narrative gets complicated.

Who’s actually in the room

The surge in “African capital” is led almost entirely by African development finance institutions — DFIs, corporates, and state-backed bodies that contributed 63% of deployed DFI capital in 2025. Pension funds, family offices, insurance companies, and sovereign wealth funds remain largely absent from the early-stage VC table.

This matters because DFIs don’t behave like commercial LPs. Their mandates come from ministries. Their risk tolerances are shaped by donor frameworks and policy objectives. Their incentives — as I’ve written before — are oriented toward procedural compliance rather than portfolio performance. Changing who holds the capital while preserving that incentive architecture changes the letterhead, not the underlying logic.

Genuine capital independence would look different: PENCOM allocating into an early-stage Nigeria fund on commercial terms; a West African family office committing as anchor LP without a DFI alongside; insurance float finding its way into venture debt. None of that is happening at any meaningful scale. The capital has a local passport. The decision-making framework largely doesn’t.

What venture debt is actually selecting for

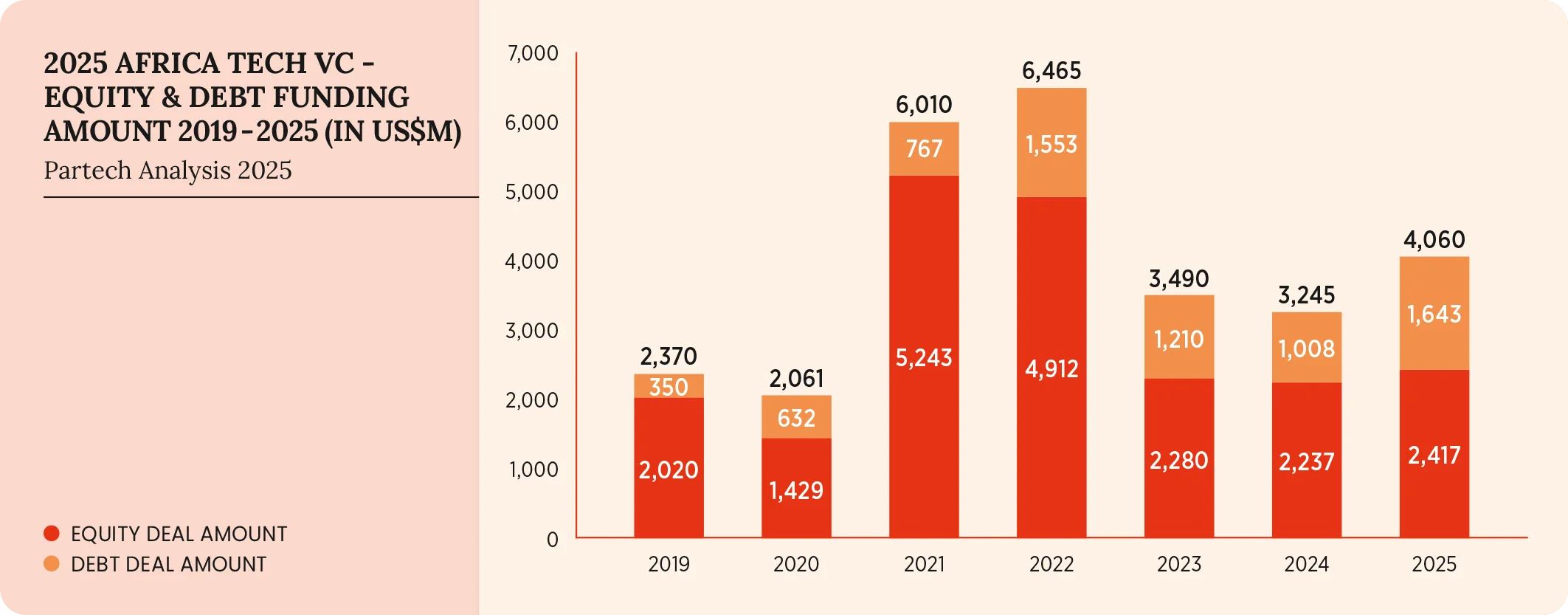

Venture debt reached $1.64 billion in 2025 — 41% of total capital deployed, up from 17% in 2019. That’s a durable structural shift, and it’s reshaping which companies actually get funded at growth stage.

Debt markets require cashflow legibility. You can’t service a loan on a growth story — you need predictable revenues and governance that holds up under lender scrutiny. Wave raised $137 million in debt against mobile money transaction volume, not a TAM slide. That’s the selection mechanism working as intended.

The growth-stage financing layer is gravitating toward companies built for durability — what I’ve previously called Camels. Not because founders suddenly became disciplined, but because the capital now available to them demands it. Lenders are enforcing what equity markets in the boom years largely didn’t.

The Nigeria number deserves attention: Kenya captured $498 million in venture debt. Nigeria received $160 million. That gap reflects FX volatility, regulatory unpredictability, and governance deficits that make Nigerian startups harder to underwrite on a debt basis. It’s a structural discount, and closing it requires policy and institutional reform — not founder coaching.

The exit number that matters more than the fundraising numbers

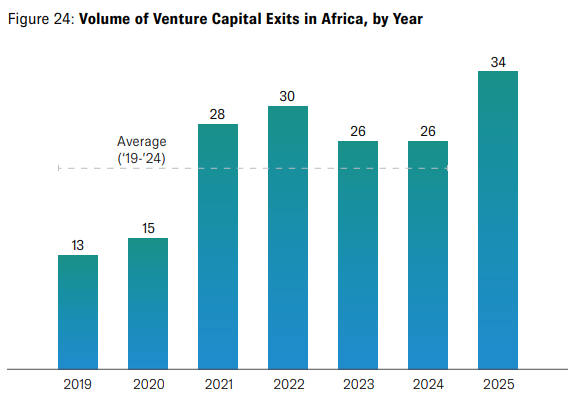

Exits rose 31% to 34 transactions in 2025. African-based buyers accounted for 54% of them.

That buyer composition is the most consequential data point in the entire AVCA report, and the least discussed. When African acquirers buy African startups, capital stays on the continent and re-enters the investment cycle. That’s how a self-sustaining ecosystem forms — not through LP commitments from development institutions, but through exits that generate local returns that local investors then redeploy. Thirty-four exits is nowhere near sufficient. But 54% African buyers, if it holds, is the right foundation.

What independence actually requires

Africa’s venture ecosystem doesn’t have a capital problem at the headline level. The deeper issue is incentive structure — who holds the capital, what governs their deployment decisions, and whether returns circulate within the continent or get repatriated.

African DFIs stepping up is progress, and it shouldn’t be dismissed. But capital independence that can survive a global risk-off cycle requires pension allocations, family office participation, and insurance capital entering the asset class on purely commercial terms. Until those pools are meaningfully engaged, the ecosystem’s exposure to external capital sentiment hasn’t materially changed. The 45% domestic figure is real. What it represents is a base to build from, not a destination.

The L.U.M.I. Brief is a weekly newsletter about African venture capital, capital markets architecture, and the structural forces shaping investment on the continent.