The Partnership That Died Without a Funeral

Why the cheap deal and the expensive one failed for the same reason

Two companies signed a strategic partnership eighteen months ago. There was a press release, a photo of executives shaking hands, a paragraph about synergies neither side ever bothered to define. Neither company can now tell you the exact date it ended, because it never formally ended. It just stopped getting calendar time. Nobody called a meeting to announce the funeral, because nobody had signed anything expensive enough to require one.

Six months earlier, a different pair of companies had finished the opposite kind of deal. Fifty pages, three law firms, a shareholders’ agreement with reserved matters and drag-along rights, a full board structure built out before either side had sold a single unit. It took four months and cost each side the better part of ₦20 million in fees. The joint venture company has generated ₦0 in revenue in the fourteen months since incorporation, because whether customers would actually pay for what the two companies proposed to build got tested after the entity existed, not before.

Both partnerships failed. Neither failure looked like the other, and that’s the part worth sitting with.

Two Failure Modes, One Cause

The instinct is to treat these as opposite problems needing opposite fixes — do less paperwork, or do more diligence. That’s the wrong diagnosis. Both deals failed for the same reason. Neither one tied the size of the commitment to the amount of evidence anyone had that the commercial idea worked.

The MOU costs almost nothing to sign. No resource changes hands, no deadline forces a decision, no metric can be missed because none was set. That’s exactly why it carries no weight — with regulators, with boards, or with the other side. Economists have a name for this: cheap talk. A signal only tells you something if it costs the sender something to send. Both companies got to tell their boards they’d “signed a strategic partnership” without either side risking anything that would sting to lose. So neither side prioritized it over whatever was actually on fire that week, and it quietly starved.

Nigerian courts generally treat this the same way, as a matter of doctrine. An MOU is presumed non-binding unless the parties can show an actual intention to create legal relations, and most MOUs are drafted specifically to avoid showing exactly that.

The joint venture agreement is the mirror image. It’s expensive enough to be a real signal, which is exactly the problem, because it got spent before there was anything to signal. Board seats, profit shares, exclusivity terms, and governance rights all got negotiated against a commercial thesis that existed only as a slide deck. Setting up the entity itself, board resolutions, CAC registration, a shareholders’ agreement, typically runs six to twelve weeks once any regulatory sign-off is involved. That’s six to twelve weeks both sides could have spent finding out whether anyone would pay for the thing they were about to spend that time structuring. The lawyers did their job well. The job itself was premature.

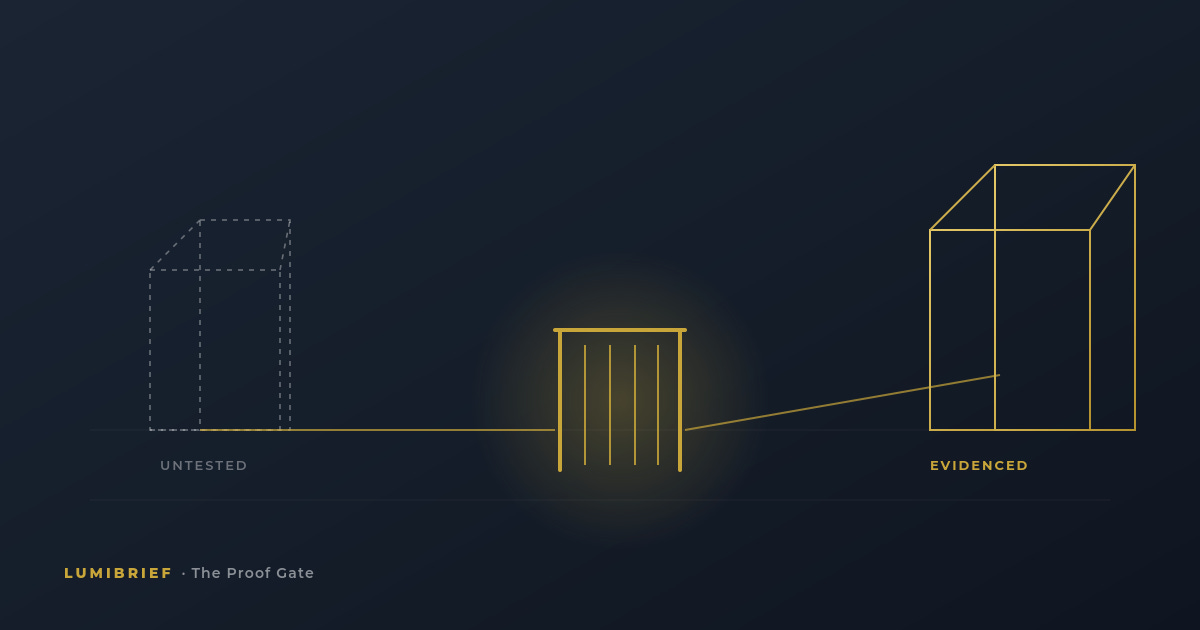

The Proof Gate

This is the model I’ve been using on recent partnership work, stripped of client specifics. Treat the first phase of any partnership as a call option, not a commitment.

A call option gives you the right, not the obligation, to buy (or buy into) something later at a set price, and you pay a small premium now for that right. Applied to a partnership, that means something specific. Instead of negotiating the full structure up front (equity splits, board seats, exclusivity, exit terms) before anyone knows whether the underlying commercial idea works, you pay a small premium instead. A short, cheap, tightly scoped pilot, in exchange for the right to build the full structure later, once there’s evidence.

The premium has to be real, though. An MOU’s premium is zero by design; a pilot’s can’t be. A pilot earns that distinction three ways, and none of them are optional. Phase 1 still carries a minimum viable set of protective terms — who owns the IP generated during the test, confidentiality, a defined exclusivity window so the counterparty can’t shop your integration to a competitor while “testing” it, a clean no-fault exit. Five pages, not fifty, but real. Before Phase 1 even starts, both sides agree a named metric and a deadline, not “let’s see how it goes” but ninety days and a specific paying customer or transaction volume, a number written down in advance. And a go/no-go date already sits on both calendars, so the review isn’t something either side has to chase.

The go/no-go date is what prevents the invisible death. An MOU dies by attrition because no date forces anyone to look at it. A Proof Gate dies, or graduates, on a specific Tuesday, in front of everyone who signed off on it, on both sides, whether the news is good or bad.

Run the arithmetic on what each path actually costs. The dead JV costs ₦15–25 million in fees plus three to six months of senior time on both sides, sunk, producing zero revenue and a governance structure nobody needed yet. The dead MOU costs next to nothing directly, but it burns something more expensive to rebuild — the credibility of “strategic partnership” as a phrase, inside both organizations, the next time someone proposes one. A Proof Gate that fails costs a small, bounded loss, plus a clean, dated answer that lets both sides move on without the slow bleed.

Apply the same ninety days the other way, and the picture changes. A scoped pilot at ₦2–4 million in legal cost, tested against a named metric, produces something a slide deck never can. A real number. Walk into the full JV negotiation with ₦18 million in verified transaction volume from the pilot window, and the ₦20 million structure is now being priced against realized cash flow, not a forecast either side can quietly walk back later. Board seats and profit shares argued over proven revenue settle faster and hold better than the same terms argued over a projection, because nobody on either side can claim the number was always going to be different.

There’s a second thing the pilot buys that the arithmetic above doesn’t capture, and it matters more than the revenue number: attribution. Walk into almost any partnership pre-pilot and ask each side privately who is actually driving the value, and you’ll get two different answers, both confident, both unverified. Take a fintech and a telco co-selling a savings product. The fintech assumes its underwriting model is the reason anyone deposits money. The telco assumes its distribution is the reason anyone signs up at all. Both walk into the term sheet believing they’re the senior partner. Ninety days in, the transaction data settles what the debate couldn’t. Say the telco’s channel produced 3,200 of the pilot’s 4,000 signups, but the fintech’s underwriting produced 71% of actual deposit volume once those accounts went live. That’s not a 50/50 partnership, whatever the original deck assumed, and Phase 2 terms (profit share, board composition, whose brand leads the marketing) should be built on that split, regardless of the goodwill estimate both sides walked in with. The same pattern shows up in music. A label and a distributor structuring a joint release each tend to credit their own marketing spend or catalogue reach for a record’s performance. A tracked pilot period settles that argument too. If 60% of streams trace to playlist placements the distributor controlled and only 15% to the label’s own campaign, that figure, not either side’s sense of its own importance, is what should set the next contract’s terms. Before the Proof Gate, both parties negotiate from the assumption that they’re the primary value driver, because neither has evidence otherwise. After it, the evidence exists, and there’s simply less left to argue about.

Who Gets to Insist on This

One honest caveat, because the model isn’t neutral to power. Whoever has more resource leverage, better alternatives, or lower switching cost gets to decide how a deal is shaped, not whoever has the better argument for phasing. A smaller company proposing “let’s test first” to a much larger counterparty can read, to that counterparty, as a lack of conviction rather than discipline — and the larger side may simply walk toward someone who’ll commit on their terms.

The way around this isn’t abandoning the model. It’s making sure the smaller side is offering something genuinely scarce inside the pilot (proprietary data, a licence, a distribution position the larger company can’t easily replicate elsewhere), so the Proof Gate reads as confidence in the asset, not hedging on the relationship. Scarcity is what buys the right to propose the sequencing. Without it, the larger party sets the terms regardless of what any deal-structuring model recommends.

There’s also a version of this that doesn’t tolerate phasing at all. Anything gated by a regulator before commercial activity can begin (a banking licence, a change-of-control approval) collapses the option value. You can’t run a cheap test of something that legally cannot happen without the full structure first. And any deal where the first exposure is itself the risk (handing over a proprietary valuation model, a royalty ledger, source code) doesn’t have a cheap version of “testing the water,” because the water is the asset. The Proof Gate is a default, not a law.

A second caveat matters just as much, and it’s not small. The protective terms inside a Nigerian Proof Gate are worth less as courtroom weapons than they look on paper. Commercial disputes in Nigerian courts commonly take up to three years to reach a first-instance judgment, which means an exclusivity clause is functionally unenforceable within the pilot’s own ninety-day window; nobody is getting an injunction before the test period ends anyway. The real deterrent isn’t the clause, it’s reputational. A counterparty who breaches a Proof Gate mid-pilot burns the relationship, and in small, overlapping markets like Lagos venture capital or Nigerian entertainment, that story travels faster than any suit would resolve. The clause is for the record; the market is the enforcement.

The real shift this argues for is sequencing, testing the partnership against a paying customer before testing it against a board committee. Most partnership work today optimizes for internal approval first: get the board comfortable, get the structure signed, get the press release out. Market validation happens afterward, if at all. The Proof Gate reverses that order, which is a harder discipline than it sounds. Internal approval is comfortable. Getting a stranger to pay for something takes actual proof.

For a platform company sitting on data, distribution reach, or a proprietary tech stack that a technology partner wants access to, this cuts the other way too. A naked pilot without IP and exclusivity terms is just a slower way to get raided, watching a counterparty extract the value of the integration and walk before Phase 2 ever gets negotiated. Size the structure to the cost of being wrong, and gate it to a date that forces an honest answer. The whole model, in one line.

Most partnerships don’t fail because the idea was bad. They fail because nobody designed a cheap way to find out early — so the expensive version got built on a guess, or the cheap version never had to answer for itself. Fix the sequencing, and the deal tells you the truth before it costs you anything real to hear it.

None of this is really about one JV or one MOU. [Africa’s private capital market moved US$5.1 billion across 530 deals in 2025] (AVCA), deal volume up 8% year on year even as total deal value fell 5%, a shift toward smaller, more disciplined transactions rather than a shortage of appetite. Africa-focused fund managers raising new vehicles saw fundraising drop 34% year on year in the same period. That’s the environment every partnership on the continent gets structured in now: less capital, chasing fewer positions, held by LPs asking harder questions about what actually converted into cash rather than what was announced. A ₦15–25 million dead JV or a slow-bleeding MOU isn’t just a bad quarter for two companies. Multiply that pattern across a market this much more expensive to raise into, and it’s the same story that shows up at portfolio level as a weak distributions number and a GP who can’t fully account for where the last fund’s capital went. The continent has plenty of partnership ideas. It doesn’t have enough cheap, honest ways to find out which ones were ever real before the capital gets spent finding out the hard way.