THE MACHINE THAT FUNDED AFRICA’S TECH BOOM IS BREAKING DOWN

The 87% collapse in African VC fundraising isn’t an Africa story. It’s a global liquidity story — and a war in Iran just made it worse.

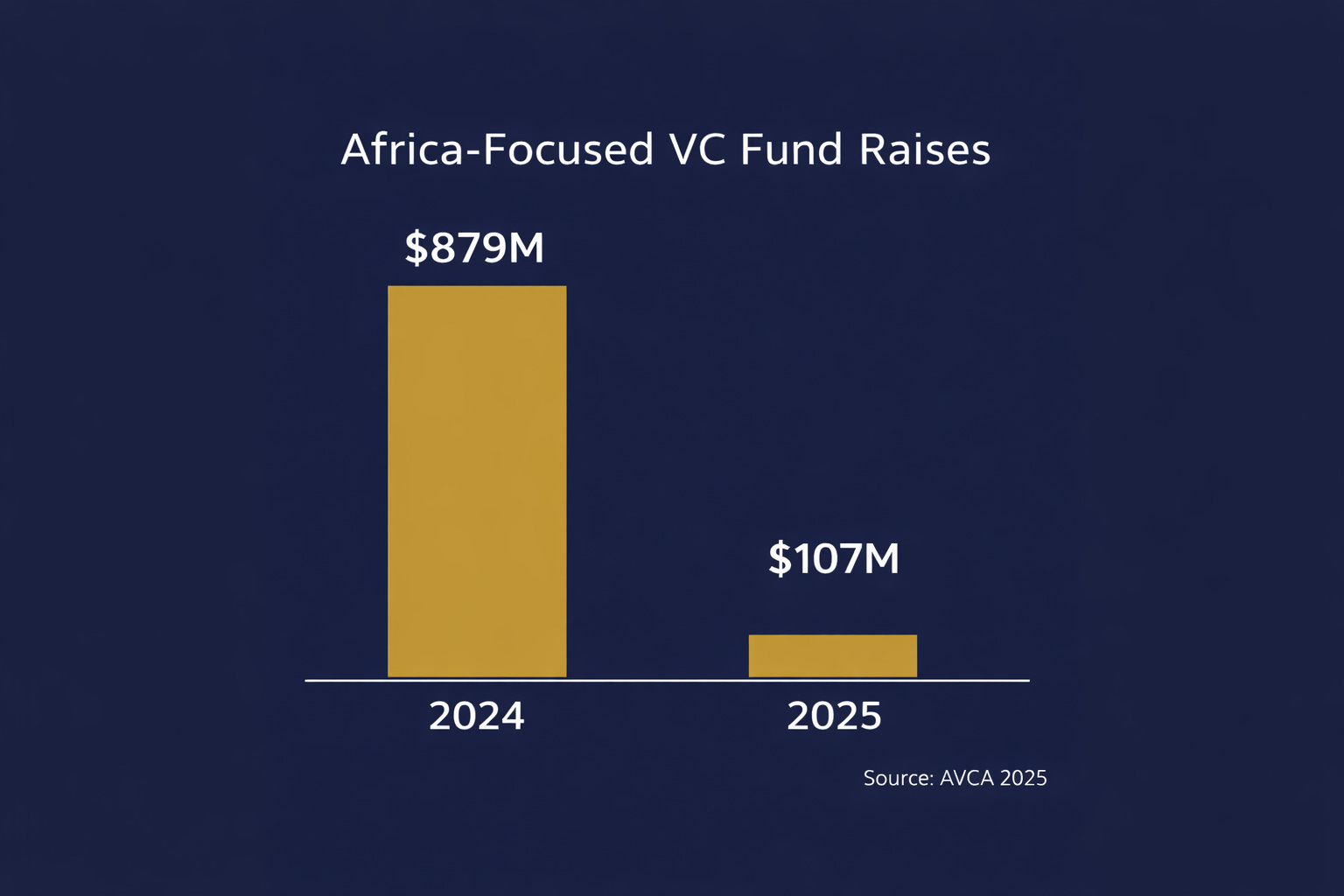

In 2025, African startups raised $3.9 billion. That number made headlines. The number that didn’t: Africa-focused venture funds raised $107 million in new fund closes across the entire year. Not $107 billion. $107 million — across all of Africa, across twelve months.

A fund close is when a GP formally collects LP commitments and locks capital for deployment. It’s the moment before the cheques get written. The $107 million figure is what the layer above African startups — the layer that builds the funds that back them — managed to raise in 2025. The collapse there was 87%, year on year.

Most ecosystem commentary is still talking about the $3.9 billion. That’s the wrong number to be watching.

Who Was Actually Funding African VC

To understand why $107 million is alarming, you need to understand who built the machine.

Between 2022 and 2024, development finance institutions — the IFC, British International Investment, the European Investment Bank, the African Development Bank and their peers — accounted for roughly 45% of commitments into Africa-focused venture funds. DFIs aren’t commercial investors. They’re state-backed institutions with mandates to deploy capital into markets that private money avoids. They anchored most meaningful fund closes on the continent. When a GP in Lagos or Nairobi was raising a $50 million fund, a DFI was almost always the first significant commitment in the room.

Around them sat European private institutional capital — family offices, foundations, funds of funds — much of it operating under the EU’s sustainable finance regulatory framework, which since 2021 has required European asset managers to classify and justify the ESG characteristics of their investments. African VC, with its financial inclusion, climate tech, and development impact narratives, fit cleanly into that system. The regulatory tailwind pulled European capital toward the asset class during the years when rates were low and yield was scarce elsewhere. DFIs and European private capital weren’t two separate engines. They were one interconnected pool, accounting for the vast majority of Africa-focused fund formation capital through 2024.

In 2025, DFI participation fell from 45% to 27% of commitments. The European private capital around them fell from roughly 70% of the fundraising pool to 21%. Not because Africa got worse — but because, across Europe, DFI mandates are increasingly redirecting toward climate finance and energy transition. Cleaner impact metrics, lower execution risk than early-stage African VC. The private capital that co-invested alongside them followed the mandate shift. Both moved simultaneously. The result was $107 million.

This isn’t a story about deals. Africa’s $3.9 billion in deployed capital held up because existing funds were still spending down commitments raised in prior years. The fundraising layer — where tomorrow’s capital originates — is a different and much darker picture.

What Built the Boom

The capital that funded African VC between 2019 and 2022 wasn’t primarily a bet on Africa. It was global liquidity overflow — excess capital seeking frontier yield when developed market returns compressed toward zero.

Low rates globally. Institutional risk appetite expands. DFI mandates widen. European impact capital chases yield. Africa gets fund formation capital. That machine ran from roughly 2017 to 2022. When the US Federal Reserve tightened aggressively from 2022, it ran in reverse — not immediately, because existing funds kept deploying and deal data looked stable through 2023 and 2024. But the fundraising layer showed the reversal first.

A GP reading 2024 deal activity and concluding LP appetite remained intact was reading the wrong gauge. Deployed capital from previously closed funds looks like conviction. It’s inventory.

Then February 28 Happened

The United States and Israel launched strikes on Iran. Within 48 hours, tanker traffic through the Strait of Hormuz — the narrow waterway carrying roughly 20% of global daily oil supply — had collapsed to near zero. QatarEnergy declared force majeure on all LNG exports. European gas storage, already at 30% capacity after a harsh winter, suddenly faced a supply cliff. The Dutch gas benchmark nearly doubled. The ECB, preparing to cut rates to support a fragile eurozone economy, paused — and raised its inflation forecast instead.

We’re now 35 days in. The Strait remains effectively closed to Western-aligned shipping. Iran is selectively granting passage to vessels linked to China, India, Russia and Pakistan. For everyone else, insurance markets have withdrawn war-risk cover, major carriers have suspended transits and roughly 2,000 ships sit stranded in the region. Analysts are modelling $150–200 per barrel oil scenarios if this persists through Q2. Q2 started four days ago and the Strait is still shut.

Why does a war in Iran matter to African VC fund formation? Because European institutional LPs — already reduced to 21% of African fund commitments — are now simultaneously managing energy inflation, rising recession probability and bond market volatility. The marginal allocation to a ten-year illiquid fund in Lagos or Nairobi is the easiest line to cut. The Iran war lands on top of a formation market already in serious distress.

The Nigeria Windfall Is Real. It’s Also Irrelevant.

Nigeria and Angola will see short-term fiscal relief from elevated oil prices. True. Also a category error when applied to the fund formation question.

Oil revenue flowing into a sovereign treasury and risk appetite in a European family office are not the same variable. One going up while the other falls is precisely the diagnosis here. An Angolan government collecting windfall revenue doesn’t make a Dutch pension fund more willing to commit to a ten-year illiquid VC structure in Lagos.

The asset class that benefits from Nigeria’s oil windfall is upstream energy equity and sovereign paper. The asset class hit by the LP psychology shock is African VC fund formation. Both are happening simultaneously. Coverage that frames elevated oil prices as good news for Africa’s tech ecosystem is conflating two completely separate things.

The Alternative Architecture Didn’t Hold

For several years, a quiet assumption circulated among African GPs: if Western LP appetite contracted, alternative capital pools — Chinese bilateral lending, Gulf family offices, BRICS-adjacent investors — could fill the gap. The events of 2026 have answered that directly.

In January, US forces seized Venezuelan oil infrastructure. I wrote about what that signalled at the time — the enforcement architecture underlying dollar-system stability, and what it meant for African capital allocation — [and you can read that analysis here]. China had committed over $100 billion to Venezuela since 2007, with $17–19 billion still outstanding. The debt was structured as oil-for-loan repayment — PDVSA ships barrels, China gets serviced. Once the US controlled Venezuela’s export revenues, the repayment mechanism ceased to exist. China hasn’t formally written it off. Beijing doesn’t do formal write-offs of politically sensitive exposure. It extends timelines, reduces visibility and waits. But the asset is a ghost. One Chinese analyst described the episode as “an almost humiliating lesson” that “the law of the jungle has never truly gone away.”

China’s response to Iran’s war tells the same story from a different angle. Not overt military support — missile components, satellite navigation access, radar systems and intelligence, covertly routed through supply chains built to evade Western sanctions — all of it calibrated to the oil supply China needs and the secondary sanctions it cannot afford to trigger. Iran stays functional. China stays insulated. There’s no BRICS collective response to any of this. There’s Chinese self-interest, finely calculated.

Gulf LP attention has turned inward. The UAE and Saudi Arabia absorbed drone strikes on their own energy infrastructure. They’re focused on their own security positions now, not expanding frontier allocations.

What looked like an alternative capital pool was a collection of bilateral transactions, each contingent on the stronger party’s interests staying aligned. For African GPs who built their LP thesis around non-Western capital, 2026 has been expensive clarity.

What GPs Raising Now Are Actually Walking Into

January and February Series A volumes at 69% below prior year. Series B: zero. Total equity capital down from 76% to 43% of deal value. Debt is up 165% because DFI mandates can accommodate a loan when equity appetite has gone. That is a totally different market, and not just a correction cycle. GPs raising their next fund right now are operating inside it: LP pools contracted, geopolitical conditions undermining DFI risk appetite, and the Iran war piling a fresh psychology shock onto an already stressed fundraising environment.

If the Strait reopens in Q2 and the ECB resumes cuts, LP psychology could stabilise and first close windows might open by Q4 2026. If the Strait stays effectively closed through Q3 — five weeks in, that’s looking less unlikely by the day — the ECB holds or tightens further and realistic first close timing shifts to H1 2027. Build the operational and cash plan around the second scenario. Pitch the first when the data supports it.

The GPs who close their next fund in this environment aren’t the ones with the best Africa story. They’re the ones who’ve updated their map — which LP pools still exist, why those LPs are still allocating, what the conversation actually needs to address. The 2021 playbook is a liability now.

The machine isn’t dead. Three point nine billion dollars moved in 2025. But the layer that assembles funds — the capital that builds the capital — is operating on a different timeline now, governed by different pressures than anything that shaped the 2019–2022 boom. The Iran war didn’t break something that was working. It accelerated the breakdown of something that had been failing quietly since 2022.

Eighty-seven percent is a loud number. Most of the ecosystem is still explaining it away.

The L.U.M.I. Brief publishes every Saturday. The paid midweek post this cycle — a GP-facing diagnostic for raising in a broken liquidity cycle — drops Wednesday.