African Music IP Has a $6 Billion Ceiling and an $80 Million Floor. The Gap Is Legal

The diligence wall sitting between African music IP and institutional capital is a chain-of-title problem — and the work to fix it precedes the work to finance it

The deal had been moving for four months. A strategic acquirer building an African catalog allocation had cleared every commercial gate. The seller, a credible Nigerian label with twelve years of operating history and a catalog the buyer’s own appraiser had valued at $38M, had signed the term sheet, opened the data room, walked the buy-side team through the artist roster in person.

Then the diligence team mapped the chain of title.

Across the catalog’s 800-odd works, the label legally owned masters on roughly 60%, publishing rights on 15%, and held only economic rights — not legal title — on the rest. The other rights sat with three offshore publishers, a defunct collection society, and in twelve cases with the original songwriter’s estate, which had never signed the assignment deed everyone in the room had assumed existed for a decade.

The deal closed at $14M against the clean subset. The remaining $24M of value did not vanish. It just became unbankable until two years of forensic legal work resolved who actually owned what.

I have been on the buyer side of this exact scenario more than once over the past three years, running diligence on African music IP for international institutional investors and strategic acquirers. Across Technolawgical Partners’ deal practice, which has been involved in a substantial body of African music IP, fund formation, and creative-economy transactions, the pattern is now stable enough to name as a structural feature of the asset class rather than an unfortunate exception. The $290M untapped African music IP lending market this publication sized in January is not gated by bank willingness, by rate compression, or by direct payment infrastructure. It is gated by chain of title.

The first $50M of that market gets unlocked by lawyers, not by lenders.

What This Means For The People Reading

Label principals holding catalogs argued at 8–12x earnings — including in this publication — are sitting on assets where the realisable institutional value, post-diligence, often lands closer to 2–4x. Same multiple gap LumiBrief has been calling for two years. Different reason. The gap is documentation, not market perception.

Banks that built credit models around the direct payment thesis are finding that Letters of Direction cannot be issued on works where the borrower’s standing to issue them is ambiguous. The January essay’s 950 basis-point rate compression assumes the letter executes. In the buy-side mandates I have run, more than three-quarters of pitched catalogs fail at the standing test before the credit team gets near the rate math.

IP funds and DFI cultural finance teams quoting the $6–10B continental catalog value figure are working off an aspirational ceiling. The realisable institutional-grade slice today sits closer to $80–150M. Not because the music isn’t worth the larger number. Because what is enforceable today is a fraction of what is claimed.

Founders and creators signing artist-label-publisher deals in 2024, 2025, 2026 are creating tomorrow’s problem. Every standard-form African contract written in this window with ambiguous master, publishing, neighbouring, and sync allocations is an unfinanceable asset waiting to be discovered in someone’s diligence eight years from now.

This essay is the seventh diagnostic in a sustained argument running through this publication over the past eighteen months. The macro layer named the eurodollar machine that funded Africa’s tech boom breaking down. The market-comparison layer named what Nairobi got right while the rest of the continent struggled — and why the enclave development model (versus national, regional or continental) model is optimal for African development. The public markets layer named the pricing failure that compounds the macro: African private rounds anchored to public market comps that no longer exist on the tape. Each diagnosed a structural defect in how capital is priced or transmitted. This one names the same defect inside a different asset class — one this publication has argued can hedge the FX dynamics that make everything else mispriced. The argument holds. The next layer down is the one that determines whether any of it can actually be financed.

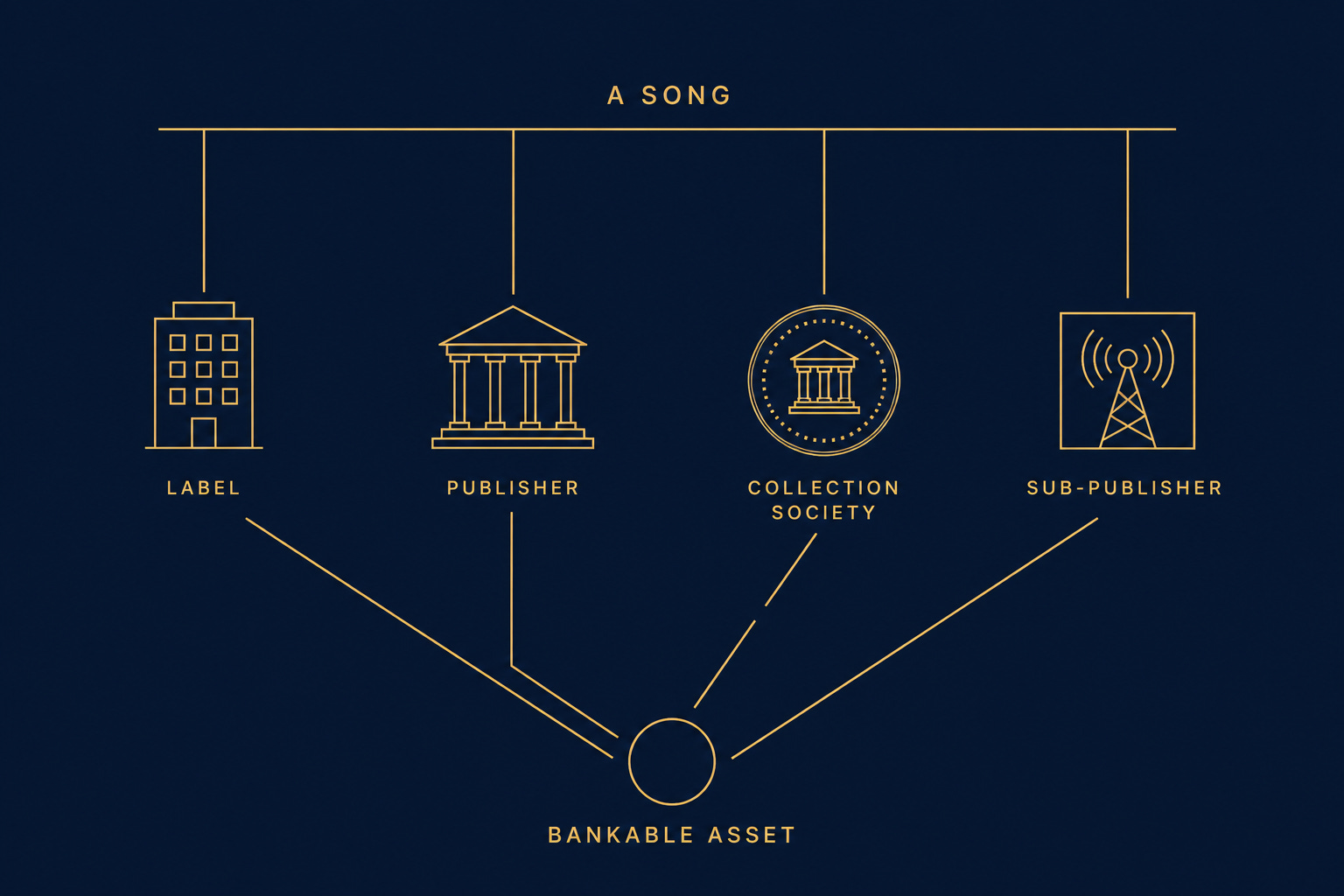

The Four Rights Problem

Every recorded song is not one asset. It is at least four.

Master rights — the recording itself, typically held by the label. Publishing rights — the underlying composition, melody and lyrics, held by the songwriter or assigned to a publisher. Neighbouring rights — performance rights collected by collection societies (in Nigeria, COSON or MCSN; in Kenya, MCSK; in South Africa, SAMRO). Sync rights — licensing for film, television, advertising, often administered by a sub-publisher.

In a properly structured Western catalog, ownership of all four flows back through documented assignment deeds to a single beneficial owner with clear standing to license, monetise, and pledge the asset. The diligence work to confirm this exists has been industrialised over forty years.

In a typical African catalog, the four rights are owned by four different entities. Three of them may not have written contracts that name the others. The economic owner — the artist or label receiving net royalties — and the legal owner, whichever party can produce a registered assignment, are frequently distinct. The party with standing to issue payment instructions on each revenue stream depends on which right the revenue is being paid against, which the platform itself may not have documented correctly at upload.

The Diligence Wall

When an institutional lender or IP fund attempts to finance an African catalog at scale, it runs four tests. In that order. Test 4 only matters if Tests 1, 2, and 3 pass.

Test 1 — Chain of Title. Can the borrower produce signed assignment deeds for every work in the catalog, demonstrating legal ownership flows from songwriter or performer to current claimed owner with no gaps? Failure looks like the opening scenario: 60% clean masters, 15% clean publishing, 25% nominal claim with no executed paperwork.

Test 2 — Standing. Does the borrower have legal standing to issue payment instructions on each work? On masters, yes — assuming Test 1 passes for that work. On publishing, often no; the publisher does. On neighbouring rights, the collection society does. Failure looks like a borrower who controls 100% of the artist relationship but only 40% of the rights that produce the revenue.

Test 3 — Jurisdiction and holding entity. Is the holding entity domiciled in a jurisdiction where the assignment is enforceable, the payment instruction is irrevocable, and security can be perfected? A Nigerian-domiciled holding entity with Nigerian-law-governed assignment deeds faces a different test than a Mauritius or Cayman holding with English-law deeds. Failure looks like a catalog held by an artist’s personal-name sole proprietorship — perfectly clean rights, no entity structure capable of receiving an institutional facility.

Test 4 — Currency basis and counterparty. Is the catalog’s revenue paid in hard currency, and through what counterparty does the payment intercept actually run?

This last test is where the January essay needs a refinement worth handling directly, because it matters operationally.

That essay framed the Letter of Direction at the platform tier — issued to Spotify, Apple, YouTube. That holds for major label and major publisher arrangements, where the platform deals with the rights holder directly. Across most of the African catalog universe, the operative counterparty for most catalogs is not the platform. It is the distributor — DistroKid, TuneCore, AWAL, Believe Music, Empire, CD Baby, Africori, Mdundo. The distributor receives the platform remittance, takes its cut, and routes the net to the rights holder.

The structural mechanism of payment intercept holds either way. The credit profile of the intercept point shifts. A Letter of Direction to Spotify is enforceable against an investment-grade balance sheet. A Letter of Direction to Africori — which since the Warner Music majority acquisition in 2022 carries a meaningful corporate backstop — sits closer to that profile than most observers realise. A Letter of Direction to a smaller independent distributor with no parent backing is a different credit instrument entirely. The diligence work has to test the distributor’s contract with the platform, not just the rights holder’s contract with the distributor. Most of the time, on the catalogs I have diligenced, the second test passes and the first does not.

The point is that direct payment is a real mechanism. The counterparty grade varies more than the original framing implied. The Wednesday companion walks through the distributor-tier specifics and how Letters of Direction get drafted differently for distributor counterparties than for platform counterparties.

What Actually Happens In The Room

Three composite scenarios drawn from buy-side mandates I have run, with identifying details removed and numbers approximate but representative.

The label that discovered it owned less than it sold. Nigerian label, twelve-year operating history, around 600 works claimed in the data room. Pitched the catalog at $35M to a regional credit fund. Diligence found assignment deeds for 380 works on master rights only. Publishing assignments for 90 works. The remaining 130 works had artist contracts that referenced “standard publishing splits” in commercial terms but had no executed publishing assignment deed registered anywhere. Translation: clean title on roughly 63% of what was pitched. Bankable catalog value at standard institutional discounts: $14–18M, not $35M. Deal restructured as a $12M facility against the clean subset, with an 18-month workstream to perfect title on the remainder. Cost of the title perfection workstream: around $280K in legal fees. Cost of not doing it before the pitch: $20M of value sitting in the room and unable to find its way into the facility.

This is the Test 1 failure. By far the most common.

The publisher whose Letters of Direction don’t stick. Pan-African publisher administering around 2,000 works. Bank attempting to finance against the publishing income stream. Letters of Direction drafted to the relevant distributors. Acknowledgements came back on 1,200 works. The remaining 800 were flagged because the underlying songwriter assignments to the publisher were either not registered with the relevant collection society, registered with conflicting splits, or registered to a different publisher entirely — residue from prior administration deals that were never properly terminated when the songwriters moved over. The Letter of Direction was technically valid. Commercially unenforceable on 40% of the catalog. Bankable revenue base: 60% of headline. The remaining 40% became a nine-month forensic clean-up before any of it could be financed.

This is the Test 2 failure. It catches publishers and administration companies most frequently, because they are accustomed to operating on commercial assumption rather than registered title.

The catalog with perfect documentation and no standing. Artist holding masters, publishing, sync, and neighbouring rights — all properly assigned, all documented, all enforceable. Pitched as solo borrower for a $4M facility against the catalog. Diligence identified that the holding vehicle was the artist’s personal-name sole proprietorship. Lender could not perfect security against an unincorporated person without exposing the artist personally to enforcement action across multiple jurisdictions. Restructure required: incorporate an IP HoldCo, assign all four rights to the HoldCo, perfect security against the HoldCo. Cost: around $15K and six weeks. Cost of not doing it before the pitch: roughly $200K in lender legal fees the artist was asked to underwrite, plus four months of additional delay.

This is the Test 3 failure. The smallest of the three categories, the cheapest to fix, but it kills deals at the eleventh hour with frustrating regularity because the holding-entity question is rarely raised in the commercial conversation that precedes the diligence.

The pattern across all three: the asset is real, the value is real, the cash flow is real. Bankability is gated by legal architecture work that has not been done.

The January essay’s 69% Year 1 return on allocated capital for direct payment lending assumes the lender deploys the capital. The capital does not deploy because the diligence wall stops most pitched catalogs from clearing the four tests. The constraint sits on the legal architecture side of the asset, not the credit side of the lender.

What This Phase Is For

The corpus has built a six-part argument over eighteen months: asset valuation, asset class framing, credit implementation, systemic capital design, development model, strategic doctrine. Every layer assumed the underlying assets were institutionally bankable in their current state. They are not, yet. The seventh layer, the one that makes the rest operational, is the legal architecture layer.

This is not a setback for the thesis. It is the thesis’s next phase.

The path from $80–150M of currently bankable African music IP to the $6–10B addressable catalog value runs through a workstream with three rough sequences. Years one and two: chain-of-title forensics and remediation across the top fifty institutionally-pitchable catalogs continent-wide. Estimated cost in legal architecture work: $8–12M. Resulting bankable AUM uplift: $400–600M. Years two through four: standardisation of new artist-label-publisher contract architecture so that catalogs created from 2027 onward are bankable by default — industry standard-form contract development, collection society interoperability work, holding-entity templates. Years three through five: securitisation infrastructure built on the cleaned base, with credit ratings methodology calibrated for African catalogs.

The $290M untapped market opens not when banks decide to lend, but when the legal architecture work is done on the asset side. The two are sequenced. Diligence remediation precedes credit deployment, not the other way around.

The label principals, publishers, and IP fund originators reading this who want to be first to the institutional capital that will follow have the same 18–24 month window the January essay flagged for the lenders. The work to do in that window is not credit modelling. It is title remediation.

What’s Next

The midweek companion to this essay will be a buyer-side field guide — how international institutional investors and strategic acquirers actually diligence African music IP, written from the experience of having run those mandates on the buy side. Useful if you are sitting on a catalog you intend to finance or sell, because the playbook the buyers will run on you is the same playbook you can run on yourself first.

For label principals, publishers, or IP fund originators who want this work done on a specific catalog before pitching institutional capital, this is what fractional general counsel engagements exist to do. A typical chain-of-title remediation runs six to twelve weeks and unlocks two to three times the bankable value of the asset. The work I have done on the buy side is the same work, applied earlier in the chain.

The asset class is real. The capital is real. The seventh layer of work to connect them is what this next phase is.