When the Banks Stop Underwriting, Someone Else Has To

The Nestoil failure is not just a banking story. It’s about who underwrites the next decade of African corporate deals — and on what terms.

Two weeks ago a corporate buyer’s CFO called me about a target they were two months into diligencing. The enterprise value model was finished, the synergy case was lined up, and the board was ready to move.

They wanted me to sign off on the loan documentation.

By the end of the call we were having a different conversation. The target wasn’t really a company being acquired. It was a balance sheet of legacy debt with an operating business sitting on top of it. Three syndicated facilities, all originated through one of the Nigerian banks now absorbing 2025 impairment charges. The buyer thought they were paying for revenue and customers. They were also paying — without knowing it — for what the seller’s lender had been deferring.

That afternoon repriced the deal by 18%. The company hadn’t changed. The underwriting market the company was sitting inside had changed, and nobody on the deal team had noticed.

Nestoil is the proximate event. The indigenous oil and gas major defaulted on roughly $2 billion of syndicated debt to a consortium of Nigerian and African banks. In October 2025 the lenders secured a Mareva injunction — a freezing order that locks a borrower’s assets across multiple institutions pending recovery — covering Nestoil’s accounts, properties, and oil cargoes across more than 20 financial institutions (Nairametrics, November 2025). The company is now in receivership and litigation.

The press is reading it as a banking-stability story. Three tier-one banks suspending dividends. About N2.16 trillion of impairment across five lenders (TheCable, May 2026). Mareva injunctions, receivership disputes in the Federal High Court.

Read at the underwriting layer, that framing misses, to my mind, the actual event. Roughly $2 billion of corporate lending demand that used to live inside Nigerian bank syndicates is unlikely to return there at pre-2025 volume in the next 24 to 36 months. Where it migrates, and on what terms, decides the next decade of African corporate finance.

Four people who should be paying attention

The GP whose 2022 portfolio company took on a Nigerian bank facility. That facility comes up for refinancing into a market where the original lender is operationally constrained for the next 18 to 24 months. Most replacement lenders I’m seeing price wider, with covenants the original facility never carried. The exit window narrows to the buyers who can absorb that capital stack.

The founder raising debt right now. AVCA data places the Kenyan venture debt market at roughly $498 million deployed in the most recent reporting year, against about $160 million in Nigeria. Comparability between the two markets isn’t exact, but the directional gap is what matters here, and that gap was already built into how the two markets are organised — I wrote about why in the DFI letterhead piece. With Nigerian bank corporate underwriting paused, the gap likely widens before it closes. The capital that fills it underwrites against your contracted revenue, not your relationship with a credit officer.

The strategic acquirer or institutional buyer sitting on dry powder. A window has opened. African corporate assets are being priced by sellers and by their existing lenders, both of whom are working off frameworks that no longer apply. Buyers who can underwrite intangibles, synergy, and jurisdiction-specific enforceability are pricing into a market the legacy banks are not currently positioned to serve.

The banker reading the 2025 results. The CBN’s forbearance unwind directive of March 12, 2026 ended the regulatory mechanism that let Nigerian banks defer loss recognition on legacy oil and gas exposures (Nairametrics, March 2026). The N21 trillion in sector exposure at end-2024 (TheCable) is now being marked. The post-forbearance market that emerges is likely to look meaningfully different from the one that preceded it.

A wider rewiring is underway. The global capital transmission system that funded the last cycle is breaking down. The work I covered on chain-of-title forensics in African music IP applied this same underwriting discipline to one of those untouched asset classes. And resilience-first venture design is among the few designs built to survive a transition like this. The Nestoil event is one node in that rewiring. It happens to be the noisiest one.

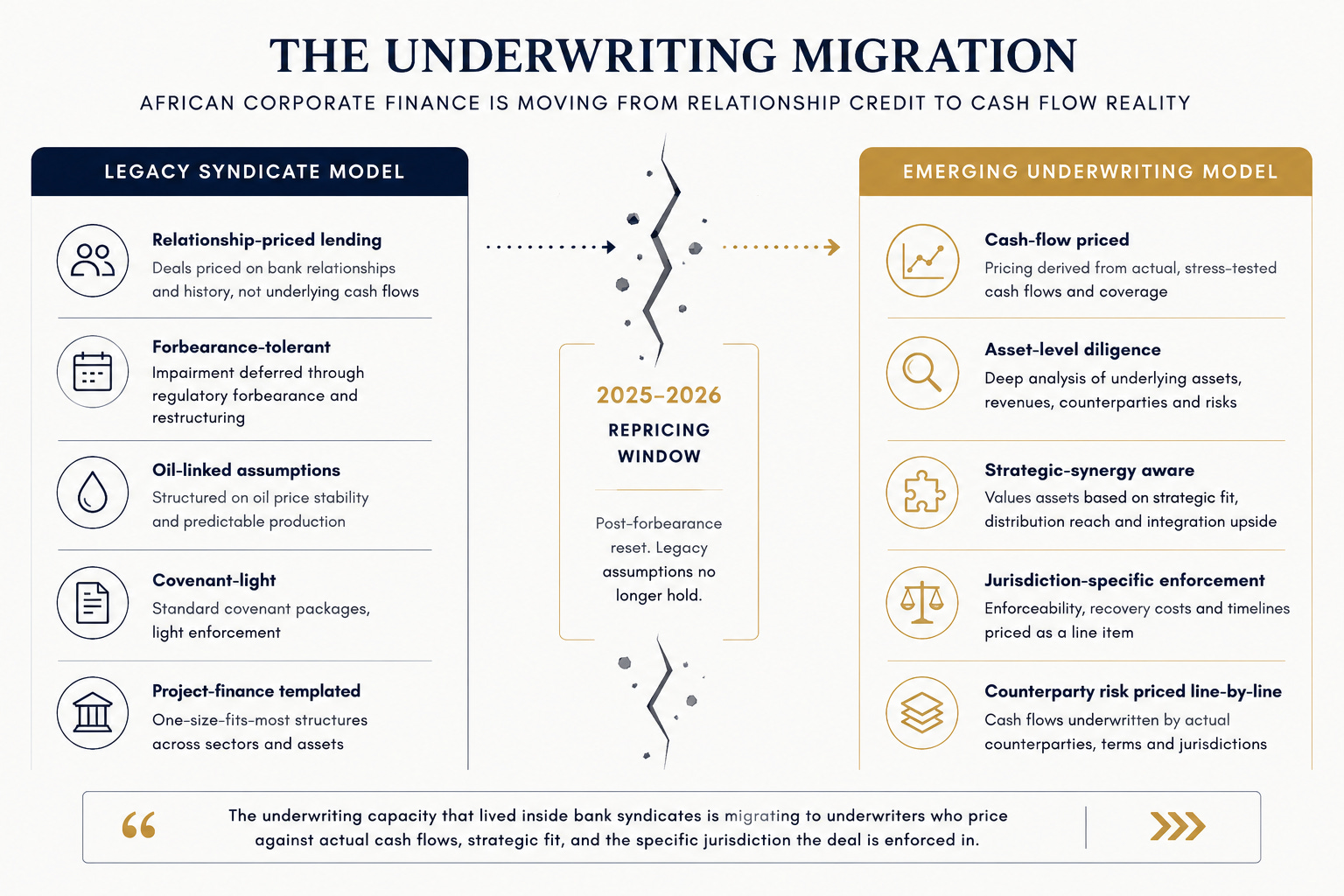

What the legacy model priced

Three things.

Relationships. The Common Terms Agreement governing the largest exposed loan was signed in 2022 (Nairametrics, November 2025). A Common Terms Agreement, or CTA, is the master contract that ties multiple lenders into a single syndicated facility — it’s where the covenants, default triggers, and inter-creditor mechanics actually live. The credit history likely sat on a banking relationship that pre-dated the 2022 CTA by years. Pricing was relationship-credit, not asset-credit. Migrating a relationship-priced loan book to a lender who doesn’t have the relationship rarely works cleanly.

Oil price assumptions. The original financing for the underlying asset was structured in 2012 around oil-price stability and predictable production. When the Forcados pipeline was bombed and the terminal went offline for sixteen months between 2016 and 2017, the syndicate didn’t reprice. Forbearance held the position for the next eight years. The loan was held at a value the asset’s cash flow couldn’t actually support.

Forbearance as a substitute for workout. The CBN’s forbearance regime let banks treat impaired loans as performing through restructuring. What it did not do was force a workout. The N3.2 trillion sector-wide impairment that hit in 2025 (Businessday, May 2026) is the price of nine years of deferred loss recognition.

What the emerging model has to price

Three different things.

Cash flows, not relationships. A music catalogue throws off royalty cheques on a specific schedule, in specific currencies, from specific counterparties. A contracted revenue book has concentration risk you can quantify per customer. A target’s working capital has FX exposure you can model per leg. Underwriting these means opening the cash flow line by line — the kind of diligence framework Nigerian bank syndicates didn’t generally need to build under the incumbent underwriting structure.

Strategic synergy. A target’s revenue is worth more inside a buyer’s distribution network than it is on a standalone enterprise value model. The corporate transaction work I’m running right now lives in this gap. The asset prices differently inside the buyer’s stack. That delta is the underwriting margin.

Jurisdiction-specific enforceability. Where a loan is enforced shapes what recovery costs and how long it takes. Mareva injunctions, receivership proceedings, eight banks in the Federal High Court in Abuja arguing about a Common Terms Agreement (The Economic Times, November 2025) — these are the post-default mechanics. The legacy model priced enforceability as a standard clause. The cash-flow-priced model has to price it as a line item.

Two scenarios from current work

The framework is easier to see in deals that are running right now. Both of the next two are drawn from buyer-side underwriting work currently on my desk — composite, with identifying details stripped out. The first picks up where the opening of this piece left off. The second extends the chain-of-title forensics work into a wider asset-class scope.

The corporate buyer.

Back to the CFO’s deal. The strategic acquirer was modelling the target on enterprise value multiples. The target’s loan book carried three syndicated facilities, all originated under a CTA that ran cross-default triggers at the parent guarantor level. Cross-default triggers mean an event of default on one facility automatically calls every other facility tied into the same CTA — the legacy lender hadn’t pulled them, but they were live.

After the March 2026 CBN directive, the practical discretion lenders had under forbearance narrowed sharply. The buyer had to underwrite to the assumption that anything that could be called could be called. The transaction price moved 18%. The target wasn’t operationally weaker. The underwriting market the target was sitting inside had repriced underneath the deal, and the buyer was the one absorbing the markdown the legacy lender had been deferring.

The 18% delta is, in my read, what the prior-cycle lending architecture didn’t price. The buyer paid it on day one of the new regime.

The institutional buyer.

An international institutional buyer underwriting a portfolio of African catalogue rights. Same diligence pattern as the chain-of-title work — every track traced back to its actual rights chain, every revenue stream traced to its actual counterparty.

The buyer’s credit committee asked the question Nigerian bank syndicates rarely asked of any oil and gas exposure. What does the cash flow actually look like, line by line, by counterparty, by jurisdiction, over a five-year horizon?

The answer required a 22-page underwriting memo. Most of it was about enforceability and counterparty risk in two specific Nigerian and Kenyan jurisdictions. A legacy bank syndicate would likely have priced the same exposure on a relationship-credit basis with a one-page covenant package and called it project finance.

The pattern across both, as I’m seeing it: the underwriting capacity that lived inside Nigerian bank syndicates is migrating to underwriters who price against actual cash flows, against strategic fit, against the specific jurisdiction the deal is enforced in. The migration is happening at deal volume, not in theory.

What the next 24 to 36 months decide

The reason this window matters is that the categories being decided in it are categories that, once set, are slow to revisit. Underwriting frameworks calcify around the deals that get done in their early years. Asset classes that get underwritten in the next 24 to 36 months become the ones that have established pricing benchmarks, recognised diligence patterns, and proven enforcement precedents. Asset classes that don’t, won’t — for a long time after.

Three things get decided in this window.

Who builds the next underwriting market is the first. The Nigerian bank syndicate model isn’t returning at pre-2025 volume in any near-term timeframe I can see. The capital that returns comes through different vehicles — international strategic acquirers, IP-focused funds, regional credit platforms, dedicated new-economy buyers. Some are already deploying; a meaningful share are still being structured.

Which asset classes get underwritten is the second. The asset classes likely to get underwritten next are the ones the legacy banking framework couldn’t price. Music catalogues. Contract receivables. Strategic acquisition targets. Hybrid debt-equity instruments tied to specific cash flow architectures. Indigenous oil and gas project finance is in multi-year retrenchment.

The third is which framework survives. The legacy framework — relationship-priced, forbearance-tolerant, project-finance-templated — is the one that produced the N21 trillion sector loan book now absorbing N3.2 trillion in 2025 impairments. The framework retires alongside that loan book. What replaces it prices the cash flow line by line, prices the buyer’s strategic fit into the asset, and prices enforceability against the specific jurisdiction the deal sits in. None of these are new in global capital markets. They are new at any meaningful scale in Nigerian and broader African corporate underwriting.

The reframe, in my read: the 2026 Nigerian corporate-underwriting reallocation isn’t the end of African corporate underwriting. It’s the beginning of the underwriting market that runs the next decade. The banks remain operationally strong — Q1 2026 numbers across the major players make that clear. What’s happening is narrower and more important: the category of large-ticket corporate underwriting that ran through Nigerian bank syndicates in the last cycle is being rebuilt, and most of the rebuilding is happening outside those syndicates.

The buyers and underwriters who price correctly into this window will be the ones intermediating the deals in 2030. The ones still working off the old framework will spend that decade explaining their losses.

The work I’m running right now sits on both sides of this. Strategic transaction underwriting for corporate buyers absorbing existing capital stacks. Asset-class-specific underwriting for institutional buyers pricing intangibles, contract receivables, and hybrid instruments where the legacy bank framework didn’t engage with the underlying cash flow.

The work isn’t about replacing the bank. It’s about pricing what the bank didn’t price and isn’t, in the near term, returning to.

If you’re sitting on either side of a transaction the legacy underwriting model would have intermediated and now does not, the conversation is worth having sooner rather than later.

[lumi@lumimustapha.com — Get in touch if you’d like a free 30-min Ecosystem Intelligence Briefing, by application only]